False Alarm: Cointelegraph's Blunder About iShares Bitcoin Spot ETF Pumped Bitcoin Price to 30K

Cointelegraph tweeted that SEC approved iShares' Bitcoin (BTC) Spot ETF, but was confirmed to be false by BlackRock.

Aaron

Aaron

Author: Luca Prosperi Translator: Deep Tide TechFlow

When I graduated from university and applied for my first management consulting job, I did what many ambitious but cowardly male graduates often do: choose a firm that specializes in serving financial institutions.

In 2006, banking was a symbol of "cool." Banks were typically located in the grandest buildings in the most beautiful neighborhoods of Western Europe, and I was looking forward to using that opportunity to travel. However, no one told me that this job came with a more secretive and complex condition: I would be "married off" to one of the world's largest but also most specialized industries—banking—indefinitely. The need for banking experts has never disappeared. During economic expansions, banks become more innovative, and they need capital; during economic contractions, banks need restructuring, and they still need capital. I tried to escape this vortex, but like any symbiotic relationship, getting out of it is much harder than it seems.

Capital Retention Buffer (CCB): Increase CET1 by 2.5%Countercyclical Capital Buffer (CCyB): Increase by 0–2.5% depending on macroeconomic conditions

Global Systemically Important Bank Surcharge (G-SIB Surcharge): Increase systemically important banks by 1–3.5%

In effect, this means that under normal Pillar I conditions, large banks must maintain a CET1 of 7–12%+ and total capital of 10–15%+. However, regulators do not stop at Pillar I. They also implement stress testing regimes and, when necessary, add additional capital requirements (i.e., Pillar II).

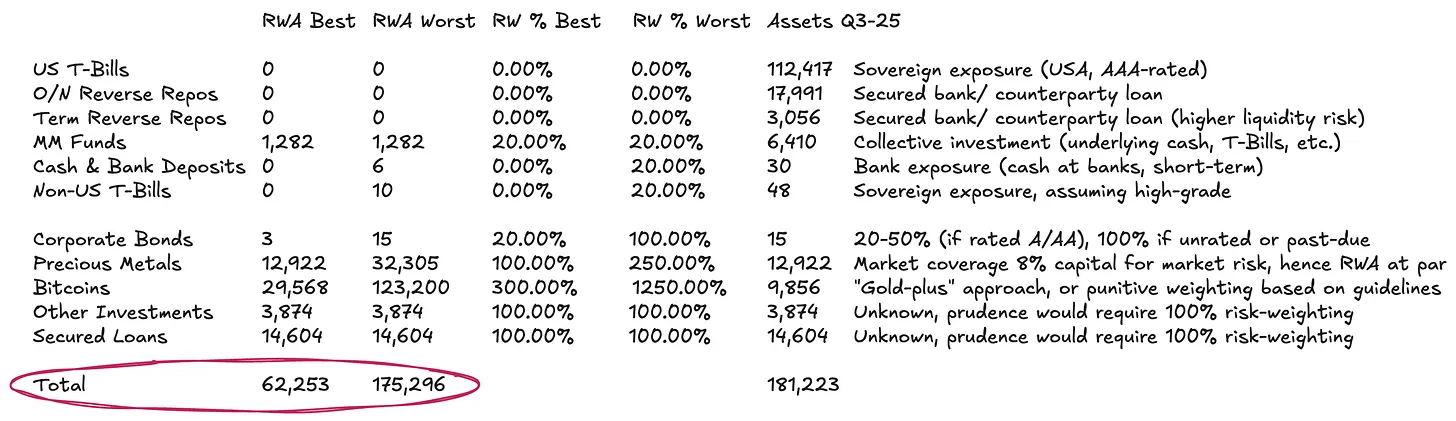

Risk-weighted classification (3), loan ledger is completely opaque. For loan portfolios, the transparency is almost zero. Since information such as borrowers, maturity dates, or collateral is unavailable, the only reasonable option is to apply a 100% risk weight. Even so, this is still a relatively loose assumption given the complete lack of any credit information. Based on the above assumptions, for Tether (USDT), with total assets of approximately US$181.2 billion, its risk-weighted assets (RWAs) could range from approximately US$62.3 billion to US$175.3 billion, depending on how its commodity portfolio is treated.

Now, we can put the last piece of the puzzle in and examine Tether's equity or excess reserves from the perspective of relative risk-weighted assets (RWAs). In other words, we need to calculate Tether's Total Capital Ratio (TCR) and compare it with regulatory minimums and market practices. This step of the analysis inevitably carries a certain degree of subjectivity.

Tether's standard rebuttal on the collateral issue is that, from a group perspective, it has a large amount of retained earnings as a buffer. These figures are indeed impressive: as of the end of 2024, Tether reported annual net profits exceeding $13 billion, and its group equity exceeded $20 billion. The more recent third-quarter audit for 2025 shows that its year-to-date profit has exceeded $10 billion.

However, a counter-rebuttal to this is that, strictly speaking, these figures cannot be considered as the regulated capital of $USDT holders.

These retained earnings (located on the liabilities side) and proprietary investments (located on the assets side) are both at the group level and outside the segregated reserves. While Tether has the capacity to allocate these funds to the issuing entity in the event of problems, it has no legal obligation to do so. This liability segregation arrangement gives management the option to inject capital into the token business if necessary, but it does not constitute a hard commitment. Therefore, viewing the group's retained earnings as capital fully available to absorb $USDT losses is an overly optimistic assumption. A rigorous assessment requires examining the group's balance sheet, including its holdings in renewable energy projects, Bitcoin mining, artificial intelligence and data infrastructure, peer-to-peer telecommunications, education, land, and gold mining and concession companies. The performance and liquidity of these risky assets, and whether Tether is willing to sacrifice them to protect token holders in times of crisis, will determine the fair value of its equity buffer. If you're expecting a definitive answer, I'm sorry to say you might be disappointed. But that's precisely Dirt Roads' style: the journey itself is the greatest reward.Cointelegraph tweeted that SEC approved iShares' Bitcoin (BTC) Spot ETF, but was confirmed to be false by BlackRock.

AaronFantom Foundation finds itself contending with a significant breach with $657K drained in the depletion of more than 35 crypto wallets.

Catherine

CatherineBut perhaps because it is always subject to attacks, and with a $50 million exploit in 2019 looming over their heads, Upbit's approach towards security and risk is more prudent than most.

Snake

SnakeThe acquisition follows a relatively recent fundingraising for BitGo and a partnership with South Korea's Hana Bank.

Clement

ClementThese exchanges have suspended deposits and withdrawals specifically for Wrapped EVER (WEVER) tokens, with native EVER tokens remaining secure and unaffected on Octus Bridge.

Davin

DavinBinance.US no longer permits USD withdrawals; asks users to convert USD to stablecoins or other digital assets.

Kikyo

KikyoThe ESMA further cautioned that even after implementation, investors should be prepared for the possibility of incurring total losses.

ClementExperience a digital gaming revolution with cryptocurrency payments in Roblox!

Hui Xin

Hui XinThe burn rate of Shiba Inu ($SHIB), the meme-inspired cryptocurrency, has witnessed an astonishing surge of more than 250% within a mere 24-hour span. This surge was triggered by a series of 23 substantial transactions, resulting in the removal of a substantial 47.9 million SHIB tokens from circulation.

Jasper

JasperSui under the investigative lens of the FSS with allegations centred on inaccurate reports pertaining to its circulating supply and the purported gains derived from staking activities.

Catherine