Terraform Labs Gains Mixed Outcomes in SEC Legal Tussle

Judge Rakoff's rulings present a complex scenario for Terraform Labs, with both favorable and adverse outcomes in their legal battle with the SEC.

Kikyo

Kikyo

Author: Prathik Desai; Translator: Block unicorn

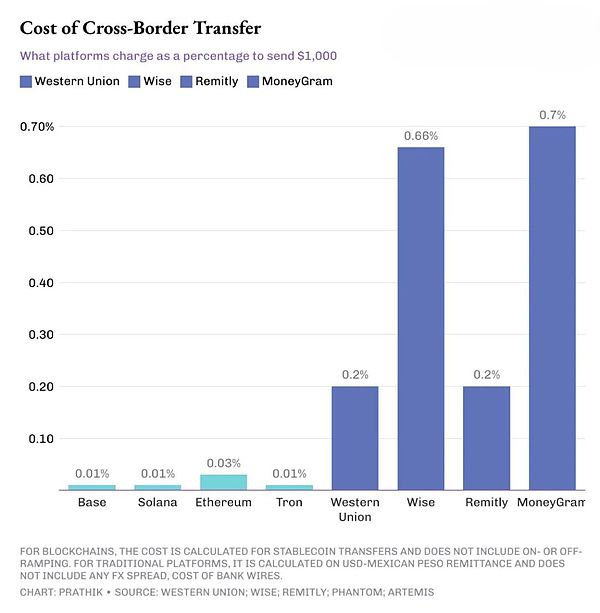

Digital paymentPayment has traditionally been slow and tedious. In the past, secure information networks (SWIFT), clearing systems (ACH, RTGS), and bank card systems could only transfer funds in bulk during business days, and we rarely paid attention to this infrastructure unless something went wrong. Users didn't have to worry about the infrastructure, but they had to pay high price differences and fees for it. Blockchain has revolutionized everything, transforming infrastructure in countries with unstable and weak economies. For example, a US company sends money to a consultant located in a South Asian or South American country. In this case, using stablecoins for payment could be revolutionary. Suppose a US company sends $1,000 to a contractor in India. Traditional remittance platforms charge 10 to 70 times more fees than blockchain platforms.

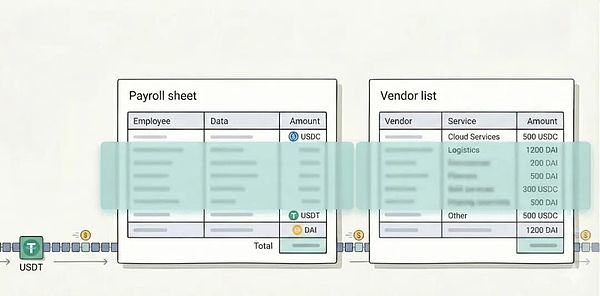

IfOutward wire transfer fee. In addition, there will be intermediary bank fees, as well as a 1.5% to 3% foreign exchange difference incurred by the receiving bank when it finally converts the US dollars into Mexican pesos or Indian rupees. This situation isn't limited to emerging economies. Even businesses hoping to receive payments from foreign clients may only see $950 or less credited to their bank accounts after receiving a $1,000 invoice. In contrast, USDC or USDT transfers on Ethereum, Solana, or Tron can be completed in seconds or minutes with fees as low as $0.30. Despite this, traditional cross-border payment platforms still dominate. Why? Because there's something more important than payment costs and transfer speed. Traditional payment systems are opaque. Payroll files are only visible to HR, finance, banks, and possibly auditors. Others can only see the inflow and outflow of funds. Public blockchains disrupt this model. When a US company pays its consultants or its suppliers in Mexico or India via USDC on Solana, anyone with a block explorer can reconstruct detailed information such as payroll ranges, supplier lists, and material costs. Addresses can be anonymous, but as I've written before, it's not difficult to reconstruct address patterns by clustering wallets into entities using tools provided by blockchain analytics companies. Therefore, when you ask a CFO why stablecoins aren't used directly for payroll and supplier payments, you'll get a consistent answer: "We can't make all internal economic activities public." If payment channels are too transparent, simply being cheap and fast isn't enough. This is why the world needs payment solutions that combine the advantages of blockchain with a privacy layer, allowing stablecoins to penetrate deeper into corporate accounting. Several protocols are currently building such chains. Stable.xyz is an EVM-compatible, Tether-backed Layer-1 blockchain that allows institutions and individuals to conduct sub-second-level peer-to-peer transfers and provides dedicated block space to ensure transaction privacy. Additionally, there's Circle's latest network experiment. Through the Circle Payments Network (CPN), the USDC issuer is working to build a closed network that connects banks, payment service providers (PSPs), and fintech companies via a single API, enabling them to transfer USDC at near-instantaneous settlement speeds while maintaining access, compliance, and risk management standards comparable to traditional finance. Celo is an Ethereum Layer-2 layer that supports stablecoin transfers with fees below cents and block times of approximately 1 second. It also offers a mobile-first user experience, supporting addresses based on phone numbers. Celo recently added Nightfall, a zero-knowledge privacy layer that enables businesses to make private B2B stablecoin payments, shielding amounts and counterparty information when needed, while also allowing for auditing. These experiments collectively aim to solve the same problem: to retain the advantages of public blockchains, such as global coverage, open access, and near-instant settlement, while also providing confidentiality for sensitive information. The adoption of these new dedicated payment blockchains is still in its early stages and the development process is not yet perfect. However, change is underway and is evident. Large financial institutions are joining this effort. During the Q3 earnings call, Circle's senior leadership mentioned that CPN had signed early cooperation agreements with several major banks, including Standard Chartered, Deutsche Bank, Société Générale, and Santander. In February 2025, Stripe acquired the stablecoin platform Bridge for $1.1 billion. This acquisition will help the financial infrastructure provider offer faster and cheaper global stablecoin trading services to businesses by integrating Bridge's technology. A simple glance at the Artemis dataset, comparing on-chain stablecoin transaction volumes with Visa, Automated Clearing House (ACH), and other traditional financial systems, reveals that the gap is rapidly narrowing. Over the past three years, adjusted stablecoin trading volume has jumped from lagging behind Visa to approximately 2.5 times that of Visa, and from a fraction of ACH trading volume to nearly half of it. The chart clearly shows that it's only a matter of time before stablecoins disrupt traditional payment systems, not whether they will happen. Looking ahead, it's worth watching how privacy-focused, payment-focused blockchains will develop. If they can settle payments via stablecoins and help businesses process payroll in bulk using a single API, then they've taken a step in the right direction. They must also ensure privacy while allowing auditors access to the information they need. That's all for today, see you next time.

Judge Rakoff's rulings present a complex scenario for Terraform Labs, with both favorable and adverse outcomes in their legal battle with the SEC.

KikyoBounce Brand's pledge pools for the AMMX token have significantly exceeded expectations, indicating robust investor confidence and innovation in the DeFi sector.

Brian

BrianJupiter Project revamps its JUP token strategy, emphasizing equitable community-focused distribution and governance.

Alex

AlexThe Indonesian government's push for crypto exchanges to register with the Commodity Future Exchange (CFX) signals a significant shift in the regulatory landscape for digital assets in the country.

Joy

JoyGlobal adoption of CBDCs, with over 130 countries involved, poses a significant threat to the US dollar's dominance in international finance. As the BRICS alliance advances alongside CBDC developments, 2024 emerges as a pivotal year defining the dollar's future amidst escalating de-dollarization efforts.

JoyOn-chain data reveals that the victim lost a total of 275,700 LINK, currently valued at $4.33 million, in two rapid transactions within a minute of approving the transaction.

BrianSingapore Prime Minister Lee Hsien Loong issued a cautionary note to the public, unveiling a concerning deepfake video circulating online. The fabricated clip, supposedly featuring PM Lee in an interview with CGTN, endorses a crypto investment platform allegedly approved by the government.

JoyZachXBT accuses X user scaredofboobs of being none other than the alleged scammer behind NFT Machine. According to ZachXBT's Telegram channel on Dec. 28, he boldly asserts, "X/Twitter User scaredofboobs is a scammer known as NFT Machine."

JoyBitcoin Cats launches Genesis NFT collection on Bitcoin Ordinals, sale on BakerySwap.

AlexWhitelisted signers gain early access to purchase SoBit's token, $SOBB, at its launch.

Brian