Binance Broadens Euro Services Through New Fiat Partnerships

After the recent withdrawal of Paysafe, leading cryptocurrency exchange Binance has announced a strategic collaboration with new fiat partners to cater to its Euro services.

Hui Xin

Hui Xin

Author: @Web3Mario

Abstract: In the previous article, we explained the risk of the Pendle PT leveraged income strategy using AAVE. Friends gave a lot of positive feedback. Thank you for your support. Since I have been studying the market opportunities of the Pendle ecosystem for some time, I hope to continue to share an observation on the Pendle ecosystem this week, that is, the real rate of return and risk of the YT leveraged points strategy. In general, taking Ethena as an example, the current potential return rate of the Pendle YT leveraged points strategy can reach 393%, but you still need to pay attention to the investment risks.

First, we need to briefly introduce this yield strategy. In fact, at the beginning of 2024, as LRT projects represented by Eigenlayer chose to use the point mechanism to determine the distribution of subsequent airdrop rewards, this strategy has attracted market attention. Users can use the purchase of Pendle YT to increase capital leverage, obtain more points, and then obtain a larger share of rewards when rewards are distributed.

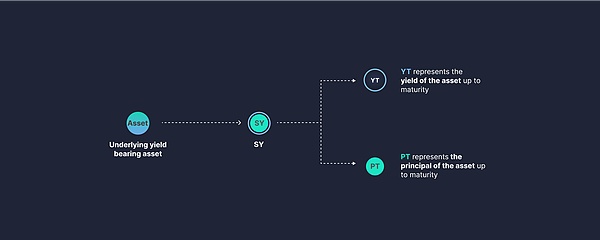

The reason why buying YT assets has the effect of increasing capital leverage is still due to the mechanism of Pendle. We know that Pendle converts interest-bearing token certificates into Principal Token (PT) and Yield Token (YT) by means of synthetic assets. An interest-bearing token can be converted into a PT and a YT, where PT is a zero-interest bond, which can be exchanged for native assets at a 1:1 ratio when the maturity date comes. Its fixed interest rate is determined by the discount ratio of PT relative to the native asset in the secondary market created by the current Pendle AMM, as well as the remaining duration. YT represents the ability of a locked interest-bearing asset to accumulate income during its duration. Holding a YT is equivalent to owning the right to income of a native asset in the future.

Since holding YT only obtains the right to income, but has no ability to redeem the principal (this part is carried by PT). Therefore, as the expiration date approaches, the residual value of YT will become smaller and smaller, until the value returns to zero at expiration. Of course, this does not mean that the value has been reduced, but part of the value has been redeemed as a reward and distributed to YT holders. That is to say, after you hold YT for a period of time, you will find two phenomena: 1. The value of the YT you hold is getting lower and lower; 2. On the Pendle Dashboard page, some of your claimable rewards appear; and the capital leverage ability of YT comes from this. Since there is only the right to income, the price of YT is much lower than 1 interest-bearing asset. Therefore, buying YT means that you can use a small amount of funds to leverage a larger scale of interest-bearing assets to capture income for you. Taking the above figure YT sUSDe Jul 25 as an example, the market price of YT is 0.0161 USDe, which means that without considering the transaction slippage, assuming that your capital is 1 USDe, you can buy 62 YT, which means that in the next 66 days, you will get the right to income of 62 USDe, which is the essence of capital leverage.

Of course, since there is no ability to redeem the principal, this strategy can only be established when the future income is at least higher than the principal invested in YT. Here we first do a simple calculation. As shown in the figure above, the current official annual interest rate of sUSDe is about 7% (funding rate dividend). Assuming that the rate level remains unchanged for some time in the future, the interest rate for users holding for 66 days is about 1.26%. However, the leverage of funds for buying YT is only 62 times, which means that investing in YT can only get a yield of 62 * 1.26%, about 78%, at maturity. This basically means that there is no additional income from investing in YT, and there is even a partial loss. As we can see from the figure, the implied interest rate and the real interest rate have recently shown a trend of convergence. However, most of the time before that, the interest rate spread was still large, which means that during that period, the price of YT may be lower, which means that the strategy is in a loss state. This is also the reason why the author did not choose to work hard on this strategy a year ago.

However, this is not the case, because when we made the above rough calculation, we ignored another source of income, that is, Point, which is actually the core purpose of YT holders to buy YT and the source of excess income.

On Pendle's Point Market page, we can see that holding YT can get point rewards for some projects. Taking sUSDe YT as an example, holding 1 YT can get 30 Sats points issued by Ethena every day. So how to effectively quantify the expected return of Point will determine the profitability of the strategy.

If you want to understand how to correctly calculate the potential point return, it is very important to clarify the point distribution mechanism of each project. Taking Ethena as an example, Ethena has conducted 3 rounds of points activities so far, and has launched the fourth season points incentive on March 25, 2025, which will last for 6 months, with a total ENA reward of no less than 3.5%. In Ethena, different sats point incentive speeds are designed for many USDe usage scenarios. The specific mechanism will allocate points on a daily basis according to the fiat currency amount of the participating scenarios, with different "multiples".

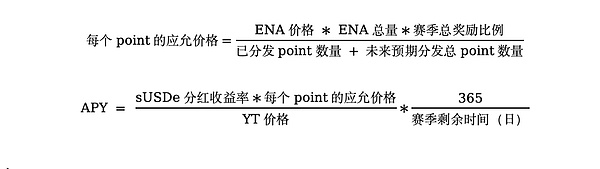

So in order to calculate the potential rate of return of investing in YT to earn points, we need to involve the following key parameters: the total amount of points currently generated daily, the points that have been distributed, the expected airdrop ratio after the end of the season, and the price of ENA at the time of distribution. Next, let's do some calculations:

1. First, we can use Ethena's official API to obtain the total number of points issued in the current season, https://app.ethena.fi/api/airdrop/stats. So far, a total of 10.1159 T sats have been distributed, for a total of 2 months.

2. Next, we can record the change in the total number of points every 24 hours, and use this to estimate how many points may be generated in the remaining time in the future if the same point release rate is maintained. Here we assume that the current point release rate remains unchanged every day, which means an average of 168.6 B points will be added every day.

3. Calculate the total amount of points that may be generated in the remaining time in the future based on your own positions. Assuming that we hold YTsUSDe assets worth $10,000, it means that we can get 10,000 * 62 * 30, which is about 18.6M points per day.

4. Combined with the current ENA price of $0.359, it is estimated that the total ENA reward will be 3.5% after the end of the season. Do the following calculation:

That is to say, assuming that you buy YT now to participate in the points competition, in the future, assuming that all conditions remain unchanged, you will get an additional 415.8% APY return on the airdrop reward corresponding to the point, a total of $13861 ENA reward. Considering the -22% loss in the sUSDe rate dividend, the total APY can reach 393%. Of course, by staking ENA, the yield of this part can be boosted by 20% to 100%, but we will not introduce it here. Interested friends can discuss with the author.

Next, let's briefly analyze the risks of this strategy. First, as mentioned above, there are five main parameters that affect the yield, the dividend yield of sUSDe, the price of YT sUSDe, the price of ENA, the total reward ratio that the project party expects to distribute in this season, and the number of new points added daily. We can use the following public statement to represent the impact of each parameter on the total annualized yield:

So how to reduce the risk of yield fluctuations of this strategy? We can roughly have three hedging strategies:

1. When the price of ENA is high, by shorting ENA, lock in the ENA price when the expected income is distributed in advance to avoid the risk of ENA price fluctuations. Of course, we must consider the margin for shorting ENA, the occupation of the principal, and then affect the rate of return.

2. In some third-party Point OTC exchanges, such as whales market, when the Point promised price is high, cash in part of the point's airdrop value in advance.

3. For the rate dividend yield of sUSDe, it can only be partially hedged by shorting major asset classes, such as BTC, ETH, etc., because we know that the funding rate of sUSDe is usually higher in a bull market, because when the bull market comes, long investors are willing to pay a higher funding rate. With the reversal of market sentiment, it is currently only possible to hedge the risk of falling rates indirectly by shorting major asset classes. However, Pendle's Boros product function allows users to hedge rate risks, so this channel is also worthy of attention.

Conclusion: This article mainly takes sUSDe as an example to introduce how to measure the benefits and risks of the YT leverage points strategy. For other targets, friends can study on their own according to this methodology, and everyone is welcome to discuss with the author.

After the recent withdrawal of Paysafe, leading cryptocurrency exchange Binance has announced a strategic collaboration with new fiat partners to cater to its Euro services.

Hui XinThe exploiter behind the exploit of BH token on 11 October, continued to evade scrutiny by discreetly depositing a total of 1,500 BNB into Tornado Cash on 19 October.

Catherine

CatherineBinance and HOPR previously announced Binance Labs' leading role in a $1 million investment round for HOPR, which precedes the company's upcoming token sale.

Davin

DavinIn a concerted effort led by Atomic Wallet, with the participation of forensic experts and centralised exchanges, a sum of $2 million suspicious deposits have been frozen.

Kikyo

KikyoCircle's new Smart Contract Platform marks a significant step towards simplifying Web3 app development for all.

Hui XinAn elaborate online scam impersonated a reporter from a well-known media outlet to conduct a fraudulent interview, tricking the victim into clicking on deceptive links that stole sensitive data and compromised his account.

Joy

JoyWilliams Racing, the British Formula 1 (F1) team, has unveiled their NFT-adorned car, showcasing non-fungible tokens (NFTs) on the rear wing. This initiative is part of their ongoing partnership with crypto exchange Kraken, which opened up a unique opportunity for NFT holders.

Aaron

AaronRyder, a cryptocurrency startup, has secured $1.2 million in funding to introduce a novel approach to safeguarding digital assets by eliminating the need for cumbersome seed phrases.

Jasper

JasperTwo weeks ago, friendtech content creators reported a surge in hacks- what's going on?

Clement

ClementSIM Swap attacks are apparently really easy- and Friendtech was the perfect target.

Clement