Ethena (ENA) to be listed on Binance Launchpool

Binance Launchpool will launch the 50th project Ethena (ENA). What is the valuation of Ethena (ENA)?

JinseFinance

JinseFinance

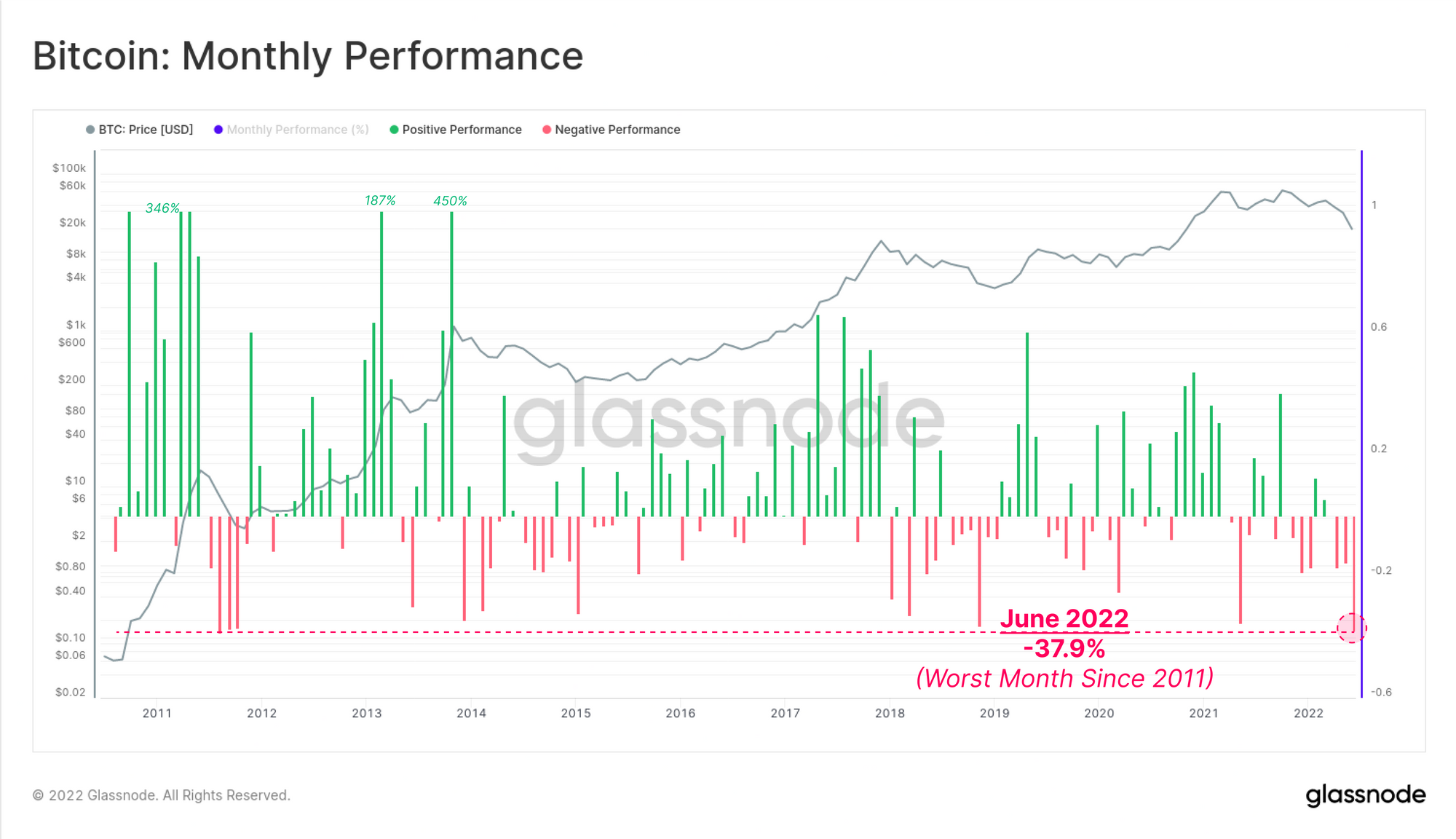

Bitcoin has had one of its worst monthly price performances in history, falling 37.9% in June. Tourists in the Bitcoin market are almost completely driven out, using the determination of the HODLer (the holder) as the last line of defense.

As the first half of 2022 wraps up, Bitcoin has locked in one of its worst monthly price performances in history. The 37.9 percent drop in prices over the past 30 days is second only to the 2011 bear market as the worst month on record. For scale, Bitcoin was worth less than $10 in 2011.

Bitcoin prices consolidated this week, paring losses for the month and remaining in a steady trading range around the 2017 all-time high of $20,000. The market opened with a high of $21,471 before falling to a mid-week low of $18,741 before bouncing back to close at $19,139.

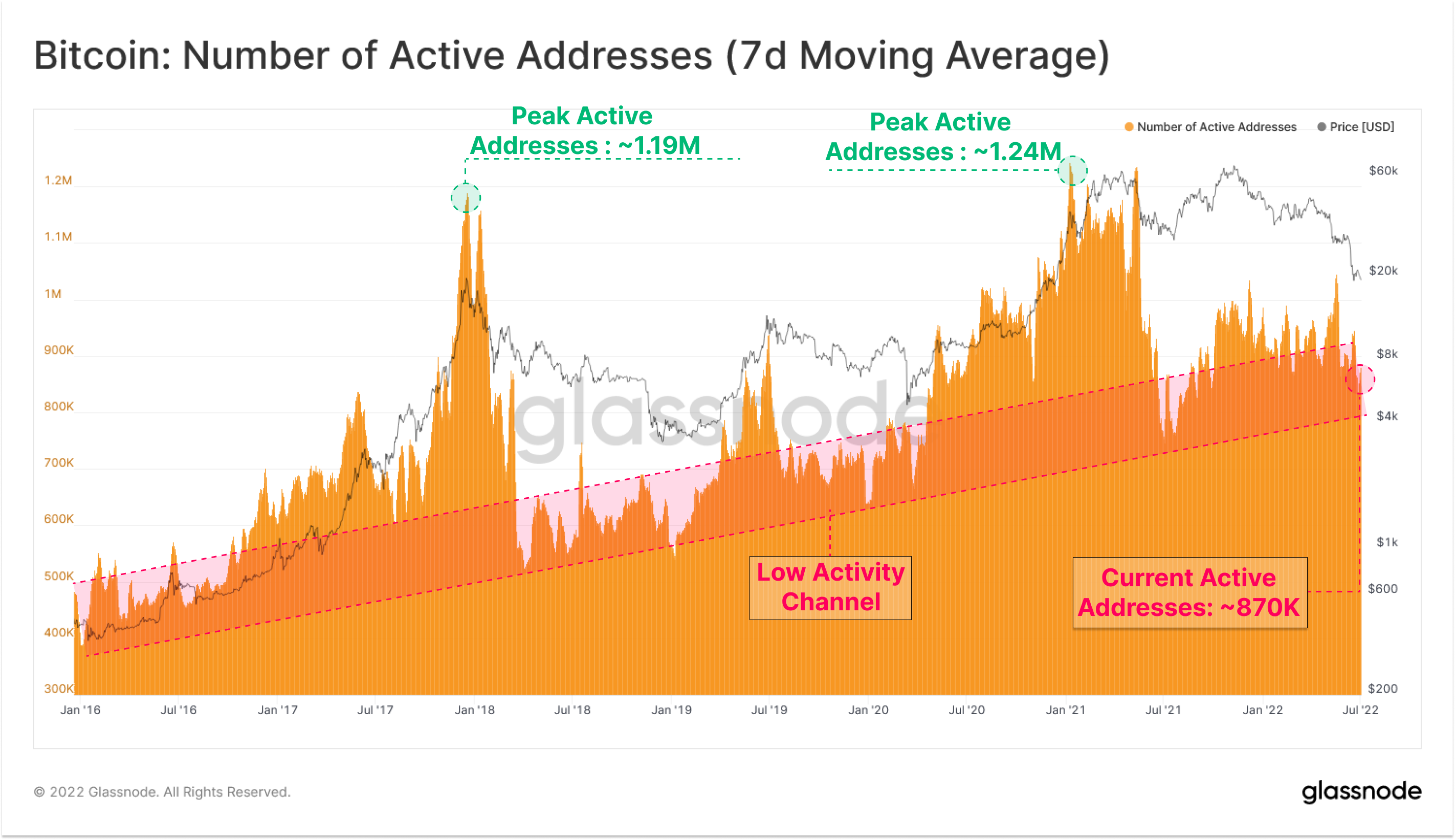

Markets remained highly risk-off as U.S. inflation expectations remained elevated in June and dark clouds loomed over a potential recession. This is evident in Bitcoin’s on-chain performance and activity, which has decreased in recent weeks. With network activity now at levels similar to those seen during the worst bear market phases of 2018 and 2019, market tourism appears to have almost completely cleared.

However, the activity that remains appears to be consistent with a determined accumulation and self-hosting trend. Exchange balances are at historically high levels, and retail and whale balances are increasing significantly.

In the face of such complex and potentially divergent market forces, in this installment we will attempt to identify the major trends emerging in Bitcoin's on-chain performance and supply distribution.

The end of bitcoin tourism

One of the most fundamental concepts in Bitcoin analysis is the assessment of on-chain activity. The concept is to identify relative strengths or weaknesses in user groups, and in particular to identify changes in macroscopic network characteristics.

High activity is usually synonymous with an influx of new demand and increased speculation, usually associated with a bull market (shown in green below).

Low activity, usually synonymous with a sharp reduction in demand and waning interest in markets, is typical of a bear market (shown in red below).

As we’ll explore shortly, nearly all indicators of on-chain activity point to network user numbers and activity approaching the deepest bear market territory in history. The Bitcoin network is approaching a state where virtually all speculative entities and market visitors have been completely purged of Bitcoin assets.

For example, address activity dropped 13% from over 1 million per day in November to 870,000 per day today. This shows little growth in new users and even difficulty retaining existing users.

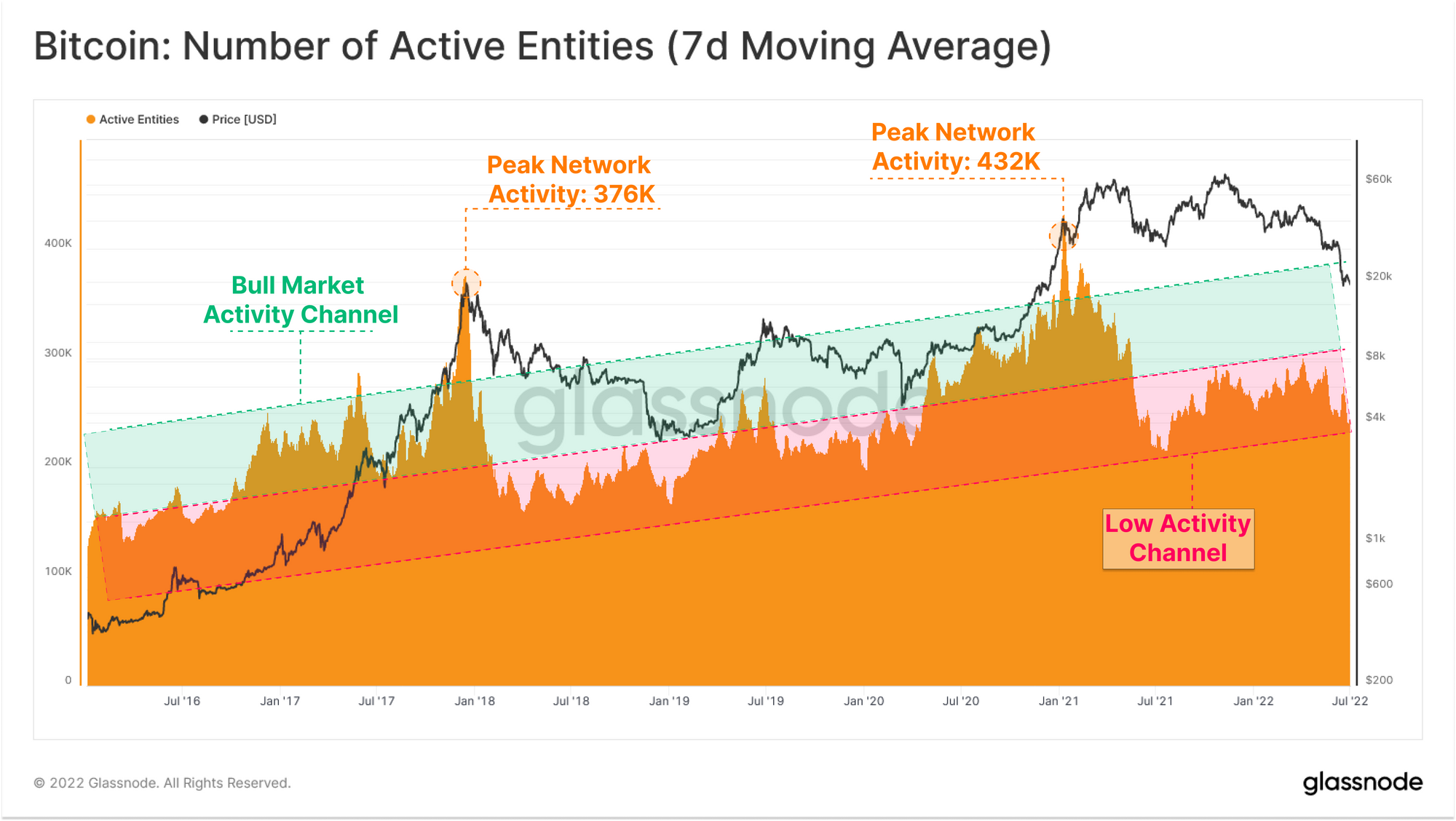

A more advanced version of this metric is the number of active entities, which benefits from our clustering algorithm. These methods collate multiple addresses and determine their on-chain entities to more accurately and clearly reflect a more likely active user base.

Active entities did experience significant gains after the November 2021 peak as participants speculated about further price increases. However, that expectation has evaporated and a general downtrend has now been established. There are roughly 244,000 daily active entities hovering at the lower end of a bear market-typical low-activity channel (shown in red).

In this metric, HODLer retention is more pronounced, with active entities generally trending sideways, indicating a stable baseload of users.

The capitulation of participants can be clearly observed through the collapse of entity net growth, which shows the difference between new entities and those that remain on-chain. Aside from two massive spikes during the LUNA crash and the late June sell-off, overall growth rates have been lackluster to say the least.

Recently, user base growth has plummeted to around 7,000 net new entities per day, which is similar to lows seen during the worst bear market levels in 2018 and 2019.

HODLer base capacity

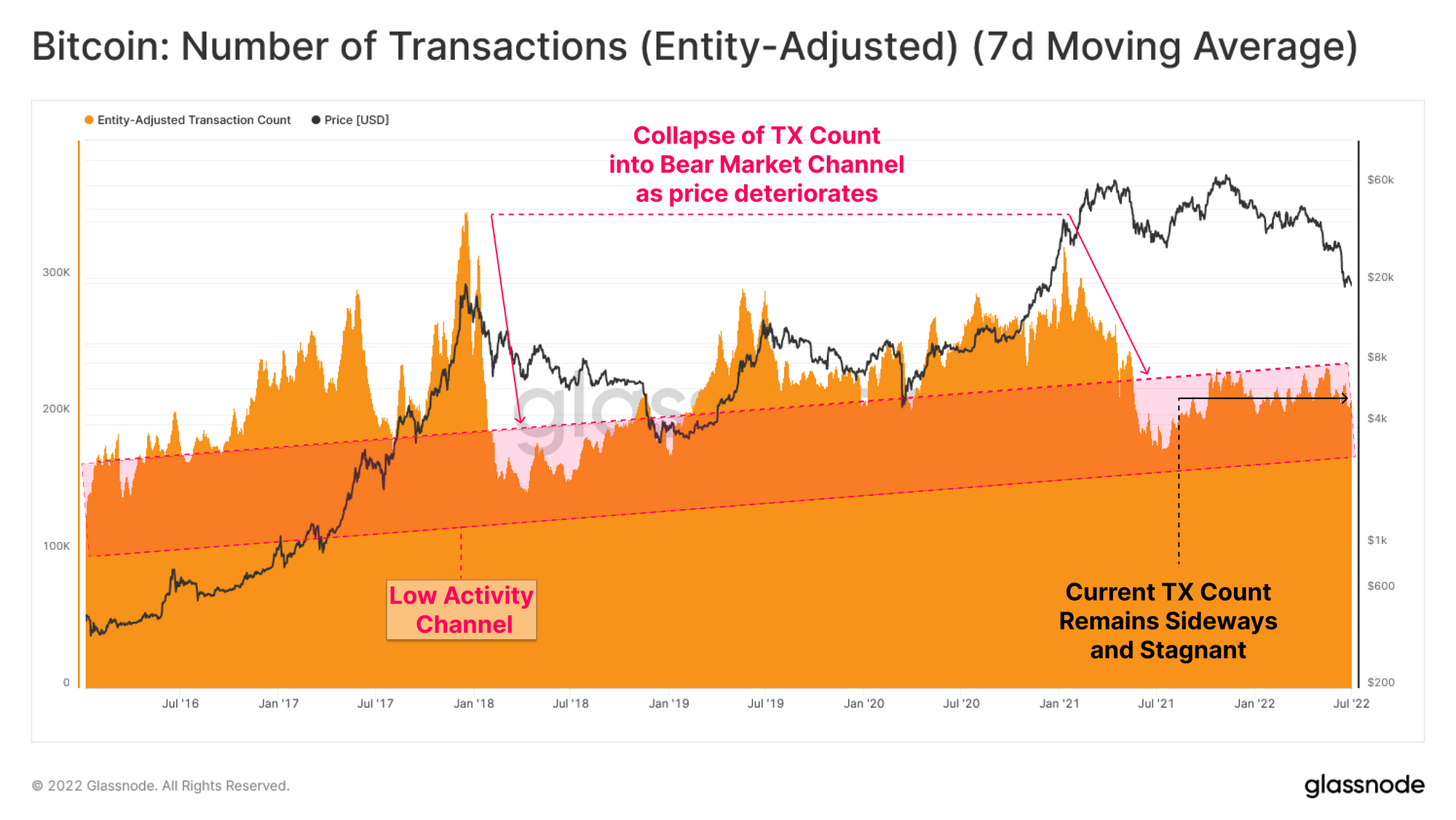

The number of settled transactions provides further insight into demand for block space and network utilization on any given day. Evaluated transaction counts are slightly different than active addresses/entities for two reasons.

At the end of the bull market in January 2018 and May 2021, the number of transactions dropped sharply. After a few months of recovery, transaction demand can be seen moving sideways throughout the main body of the bear market. This indicates both a stagnation in new incoming demand and a possible retention of base loads for users (HODLers).

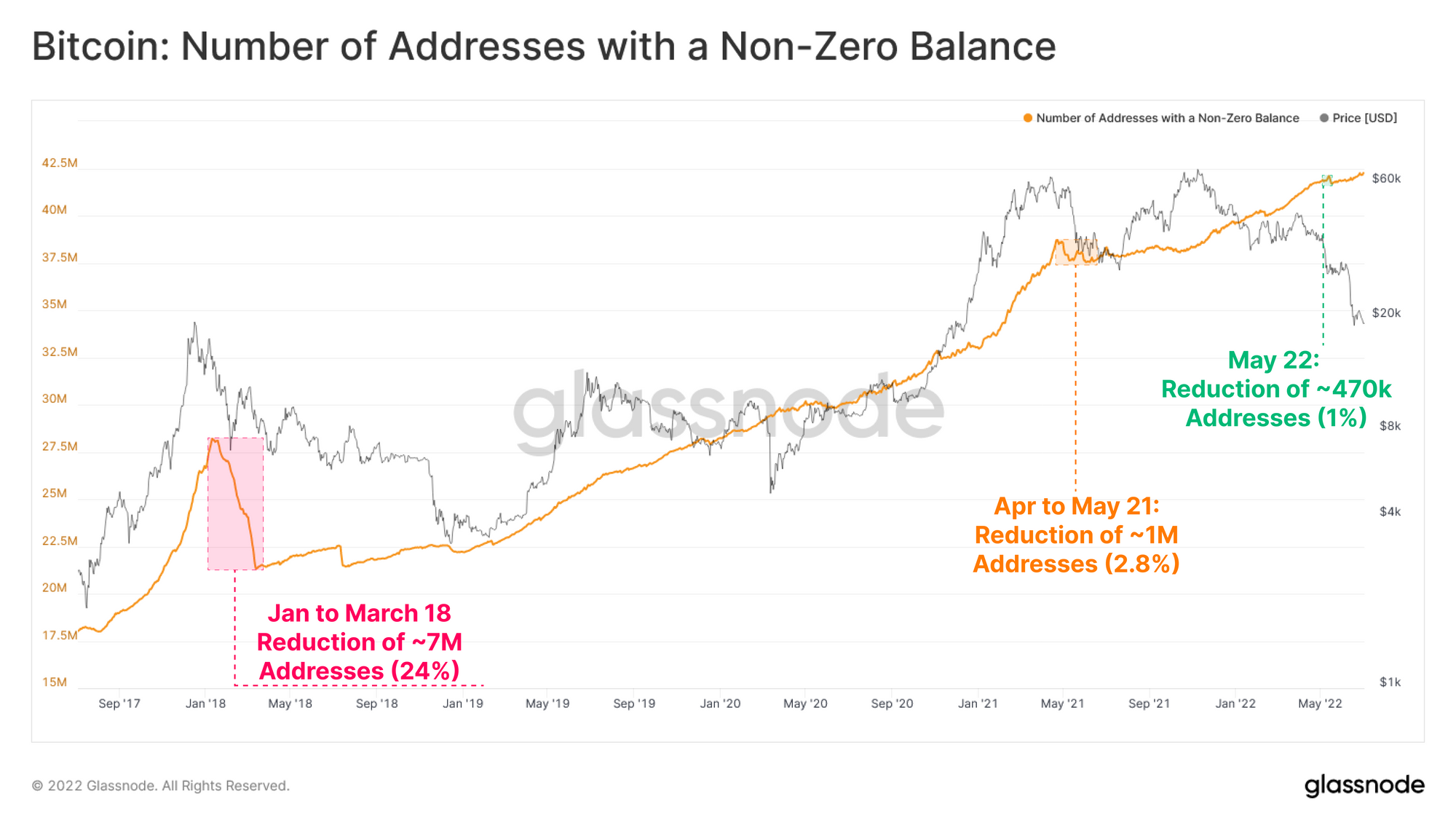

Reinforcing this, the number of addresses with non-zero balances continues to rise, reaching a new high of 42.2 million, and has been minimally affected by the recent capitulation.

During sharp sell-off events and early bear markets, the Bitcoin network often sees massive wallet washes as investors capitulate and spend all their money.

After 2018, it can be seen that the severity of non-zero address capitulation has decreased, indicating an increasing level of determination among ordinary Bitcoin participants.

On-chain activity remains severely depressed and is convincingly in bear market territory. Over the past 12 months, almost all marginal buyers and sellers appear to have finally capitulated and been purged from the network. This leaves only the baseload HODLer with the highest resolution. There is little support on the demand side of Bitcoin, so the price is correcting until these HODLers can make a firm bottom.

deal divergence

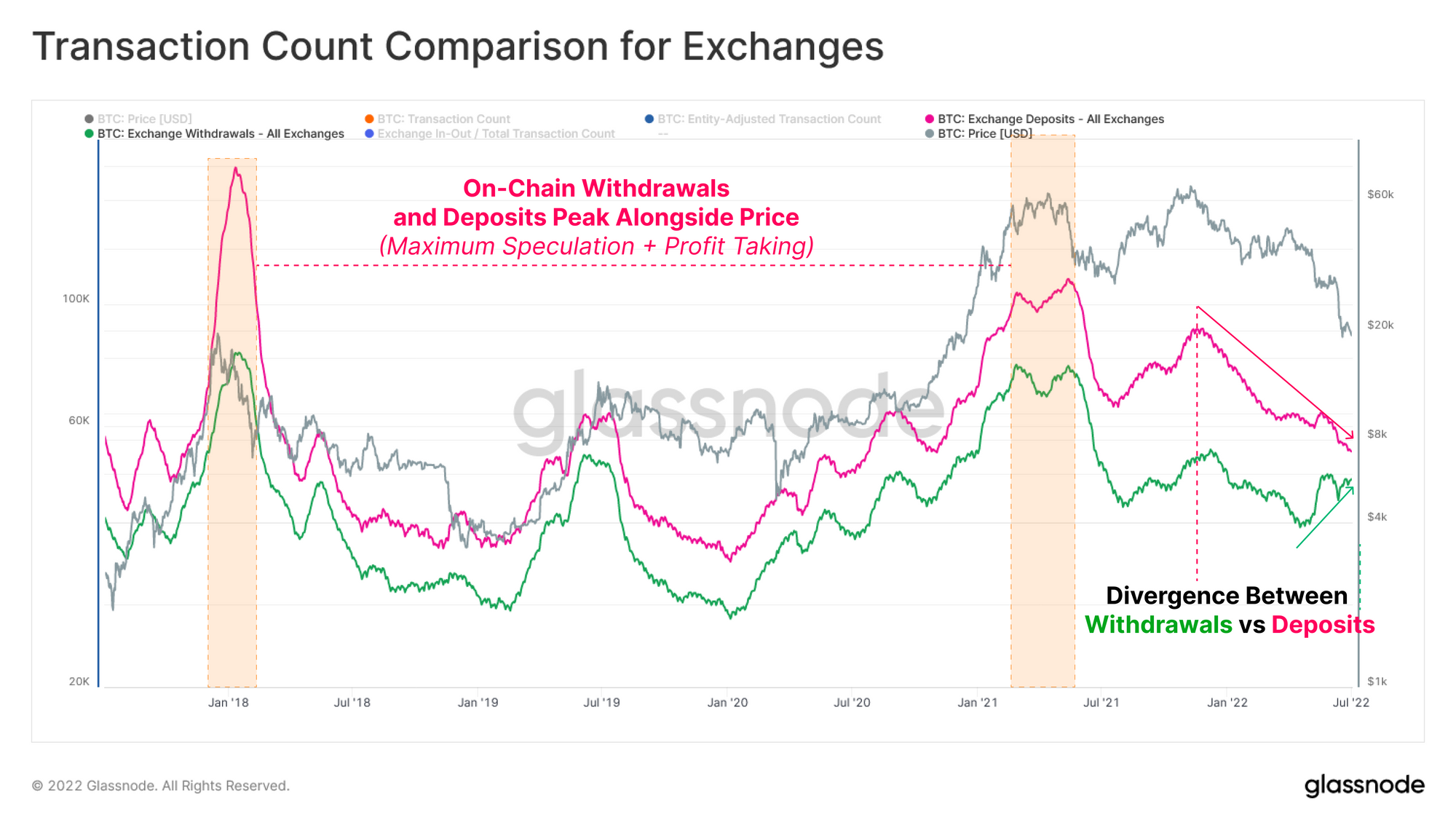

Exchanges remain at the heart of the bitcoin market infrastructure, with hundreds of millions to billions of dollars in bitcoin value flowing through the chain every day. The amount of exchange deposits and withdrawals often shows a high degree of sensitivity and correlation with spot prices.

Generally speaking, both deposits and withdrawals follow price action, peaking at bull market tops when speculative demand inflows are highest. Withdrawals (green) are usually less than deposits (pink). This is because exchanges process withdrawals from multiple clients in one transaction, while deposits are processed separately.

In recent weeks, there has been renewed focus on self-custody of blockchain assets, with some lending services suspending user deposits and withdrawals. Perhaps in response to this unfortunate event, we are currently seeing an increase in exchange withdrawals, while the number of deposits continues to decline.

This is historically unusual and there have been few examples of it in the past 5 years.

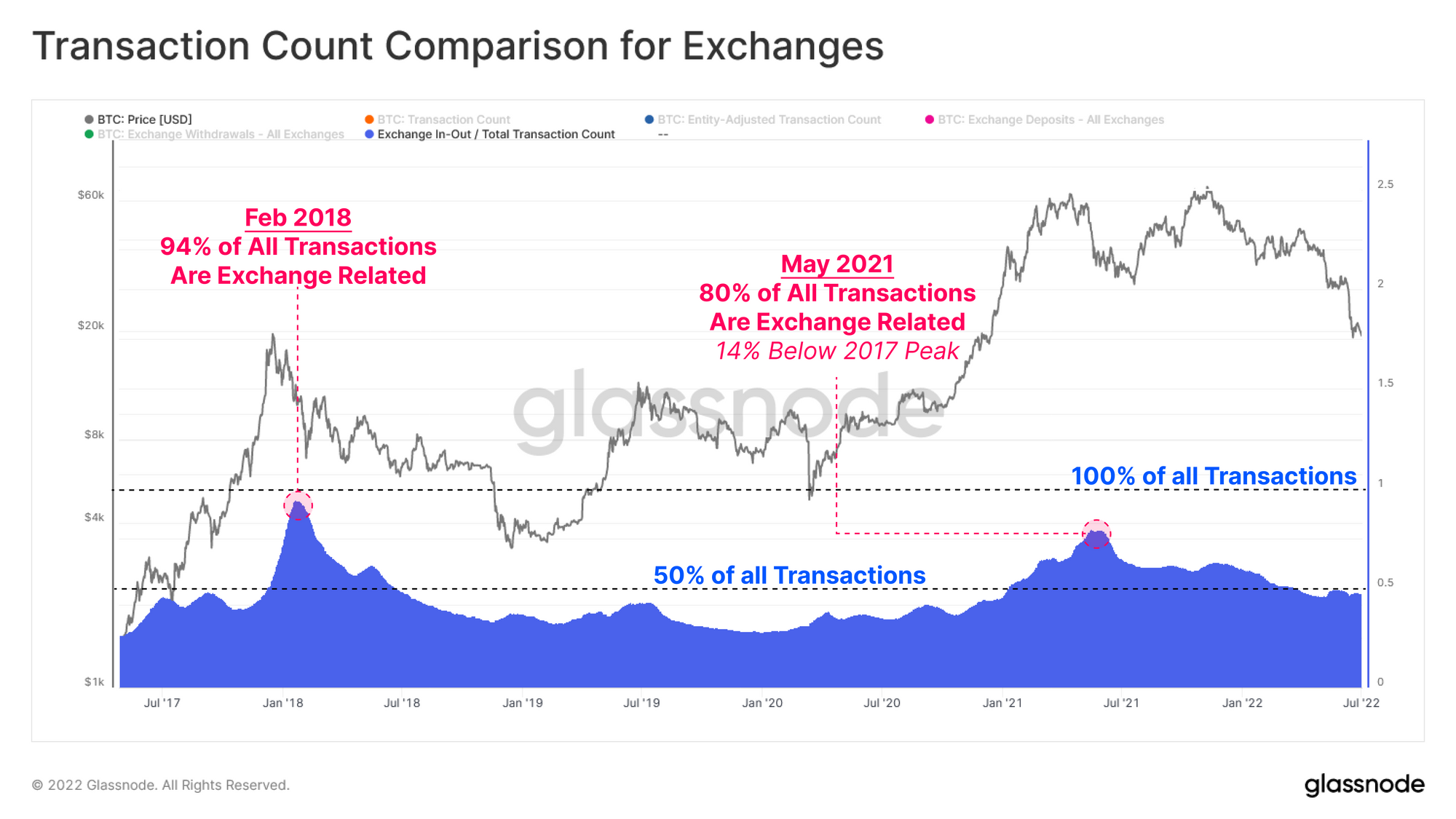

We can also evaluate the dominance of exchange-related activity as the ratio of all transactions across the network. From this we can identify peaks and troughs in investor activity and identify changes in the baseload market structure.

After the bull markets peaked in 2017 and 2021, exchange trading dominance peaked almost immediately, accounting for 80% to 94% of all activity. This marked the last gasp and influx of market tourism, as new entrants bought at the top before prices crashed, and they were subsequently ejected from the network.

Exchange-traded dominance has experienced prolonged dilution since the May 2021 high and appears to be stabilizing at around 50%. This supports our previous observation that the market is approaching HODLer dominance.

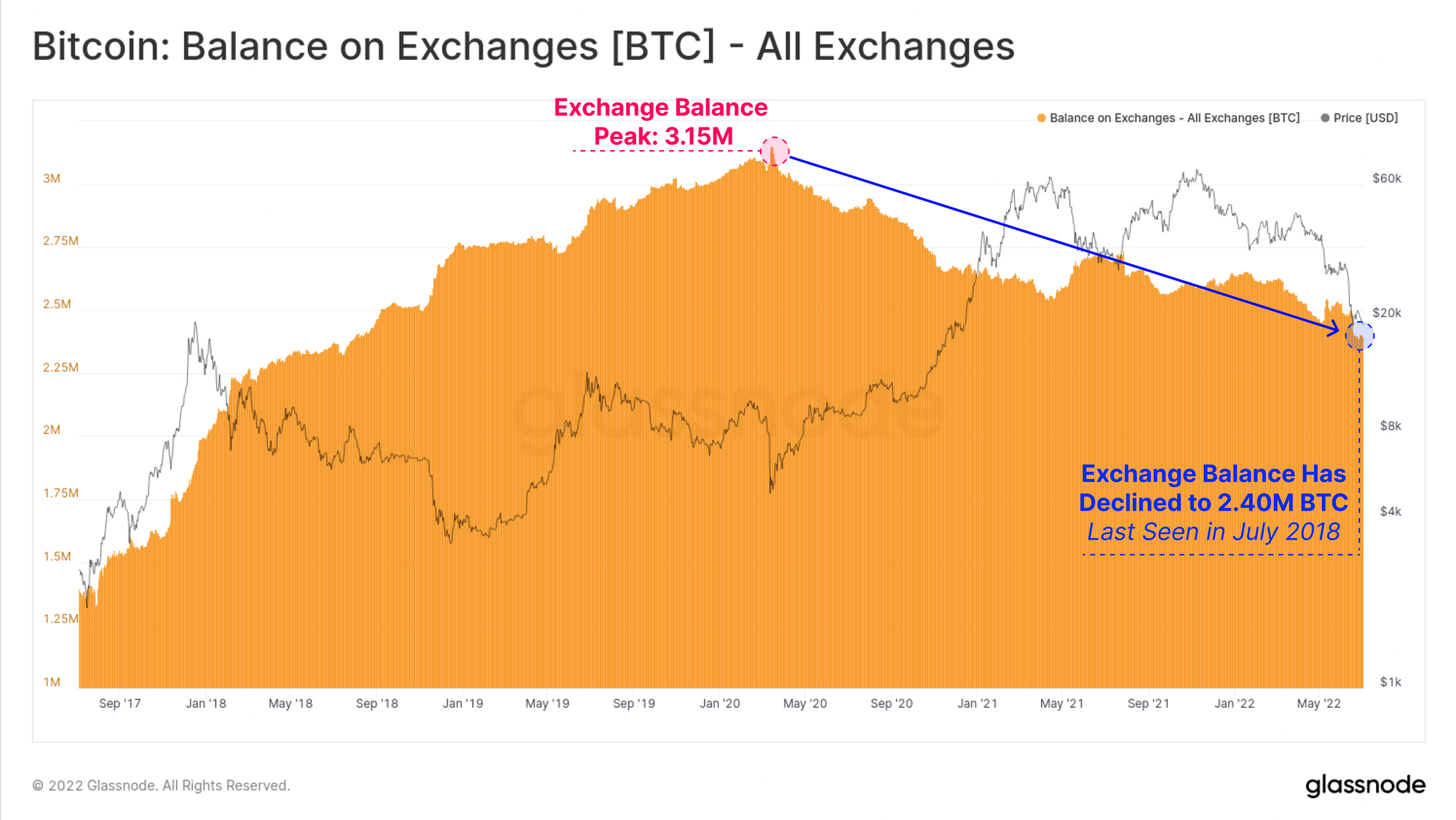

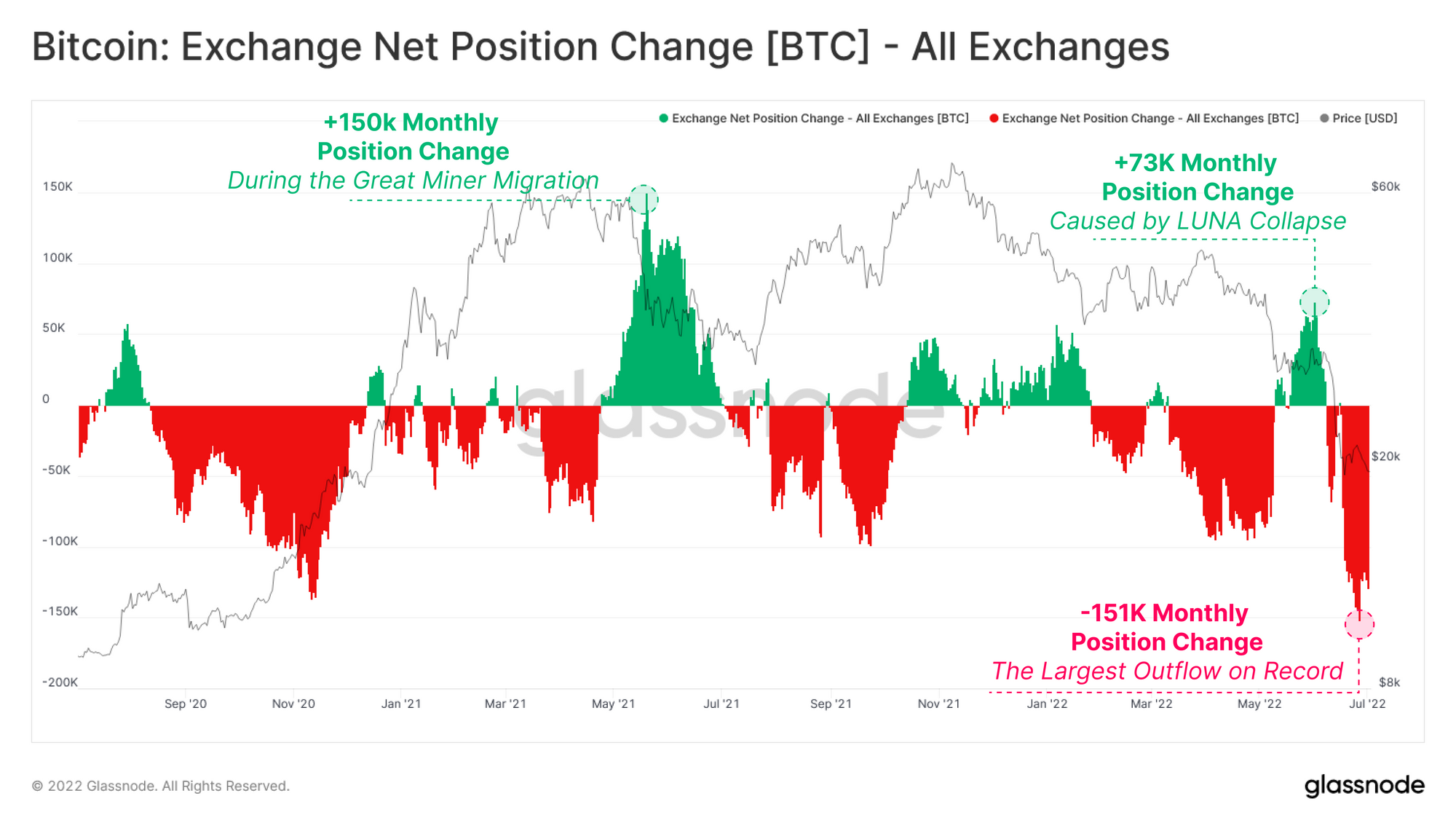

Exchange reserves continued to see massive net withdrawals, with total balances falling to their lowest level since July 2018. Since March 2020, 750,000 BTC have been withdrawn from the exchange’s total balance. In the past three months alone, 1.425 million bitcoins have flowed out, accounting for 18.8% of the total.

Exchange outflows of this magnitude, especially in the face of such extreme price downside moves, are interesting, and we will break down these flows further in the next sections.

We can watch these reserves change across individual exchanges, and we see an interesting divergence happening:

In addition to a historically poor month of price performance, the exchange also saw its largest monthly drop on record with an outflow rate of 150,000 BTC/month. This resulted in a 5.0% - 6.0% reduction in the overall June balance. This is in stark contrast to the massive influx of tokens into exchanges that occurred in May-June 2021.

Where did all the tokens go?

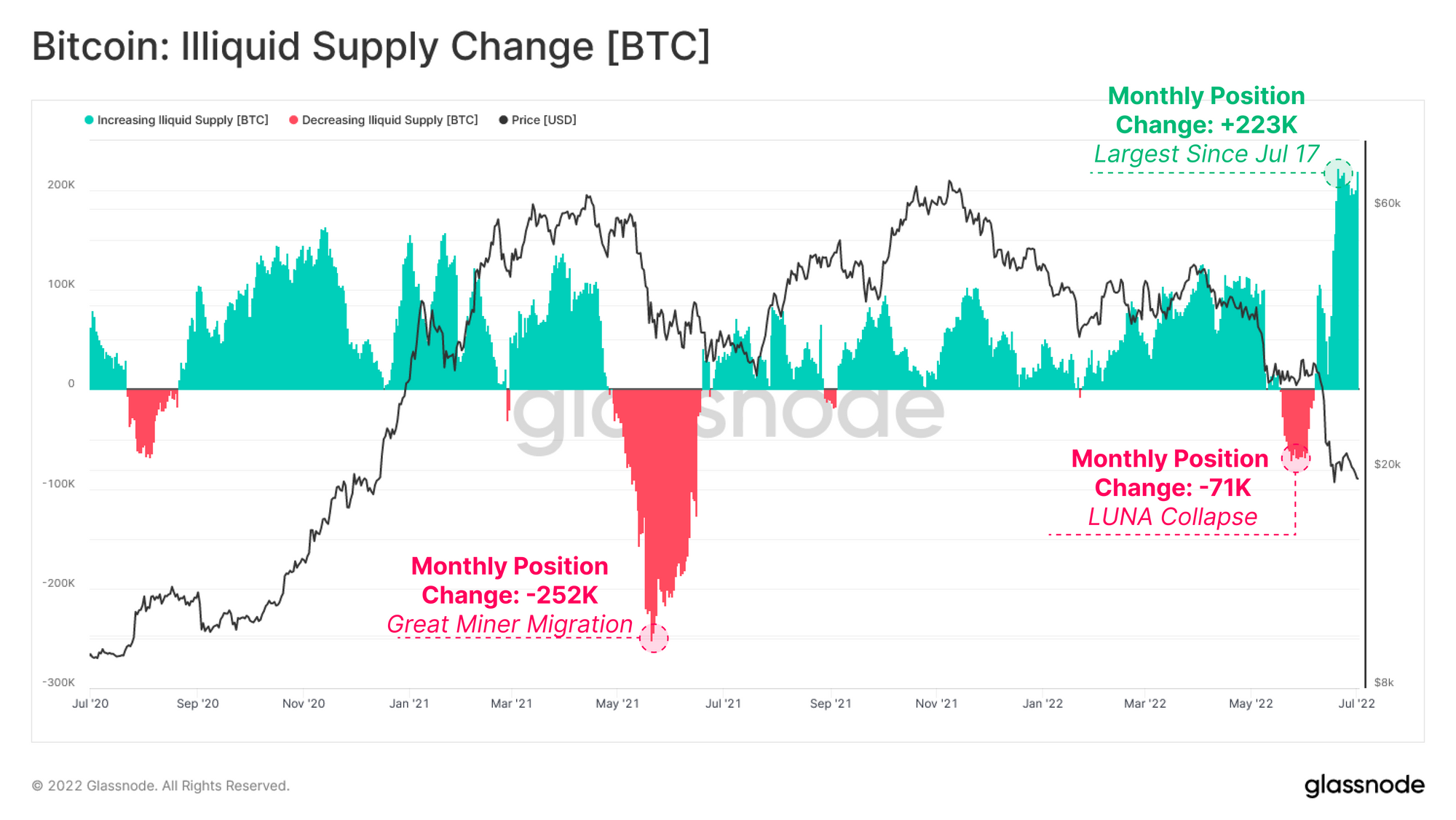

The largest change in illiquid supply since June 2017 complemented the largest change in exchange net positions on record. In July, the illiquid supply increased by 223,000 BTC, reflecting a massive flow of tokens to wallets with little to no spending history (generally. These are not transactions).

Again, this is in direct contrast to May 2021 and during the LUNA crash, both of which saw a collapse in price and a collapse in illiquid supply.

As the total exchange volume continues to dry up, we could see the largest (10k+ BTC) and smallest (

The group holding 10 to 10k BTC is almost completely neutral, with no significant change in their total holdings.

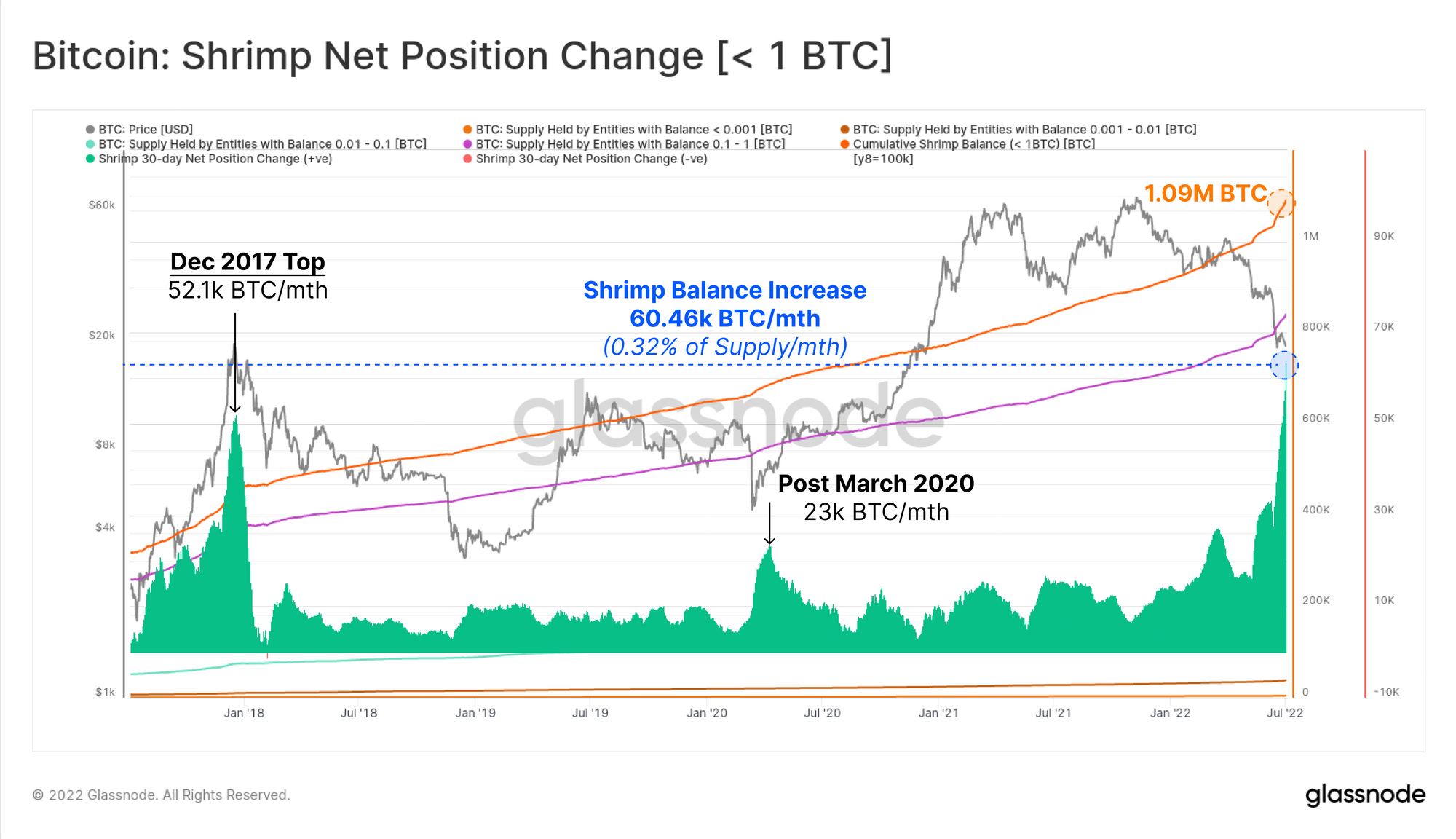

Digging into this, we can see that retail balances are increasing at a rate of 60.46k BTC per month, the most aggressive rate in history. This equates to 0.32% of the monthly circulating supply. Interestingly, retail balances expanded faster than the previous record set at the December 2017 ATH, which was also at $20,000.

The retail investor community clearly sees $20,000 as an attractive price, even though the market is trending against it this time around.

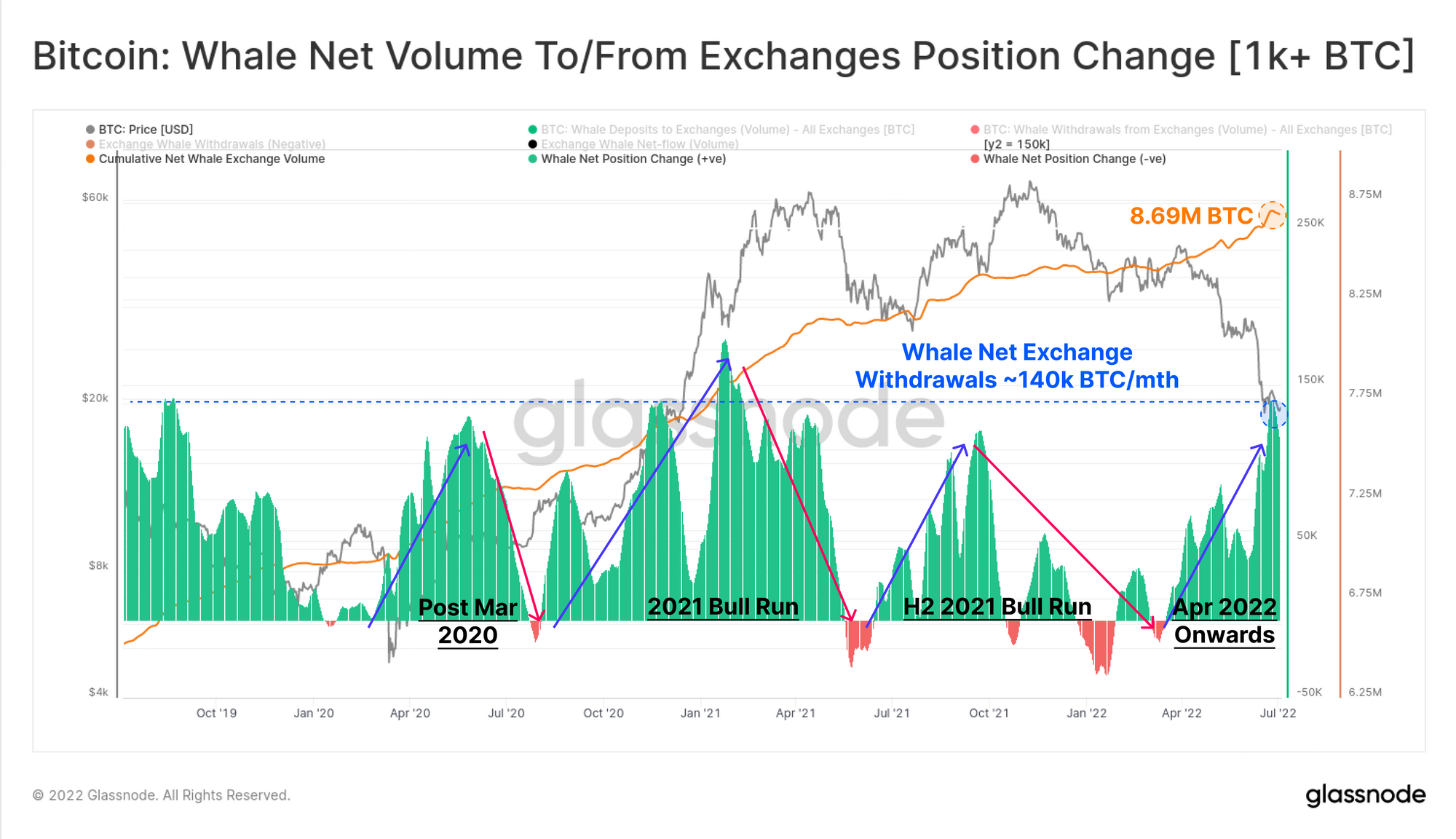

Finally, the graph below is derived from our Whale to/from exchange volume metric, where whales are defined as entities with >1000 BTC (excluding miners and exchanges).

In net worth, whales have withdrawn 8.69 million BTC from the exchanges we track, and their accumulation and distribution cycles appear to be closely tied to market price performance. Since April 2022, whale trading volume has been dominated by withdrawals, reaching a significant level of 140,000 BTC/month in June. This is the second highest level in the past 5 years, after the January 2021 pullback.

in conclusion

Bitcoin on-chain activity is in bear market territory, with recent network utilization suggesting an almost complete removal of all market visitors. Demand for block space is low, and network user growth has been lackluster at best.

Beneath the surface, however, the market is experiencing a number of very interesting divergences. The strong HODLer tone remains despite a historically poor year-to-date, which is now the worst month for prices since 2011.

Exchange reserves continue to drain as participants find new momentum in self-custody. These tokens appear to be flowing into wallets with no spending history, while both retail and whale groups are seeing historically aggressive balance growth and exchange withdrawal activity.

The Bitcoin bear market is in full swing, and in the aftermath, the "Holders of Last Stand" (HODLer) are the last survivors.

Original source: https://insights.glassnode.com/the-week-onchain-week-27-2022/

Binance Launchpool will launch the 50th project Ethena (ENA). What is the valuation of Ethena (ENA)?

JinseFinanceThe decentralized exchange holds over $390 million in locked tokens as of Tuesday.

Coindesk

CoindeskBitcoin has been declared 'dead' 463 times. Is the S2F price prediction model still valid?

Beincrypto

BeincryptoThe new game, dubbed Club Bitcoin: Solitaire, aims to increase bitcoin adoption by specifically targeting female audiences and emerging markets.

CoindeskCristóbal Balenciaga’s never-before-seen drawings inspire the new NFT collection through a collaboration between Cointelegraph, Art Consulting, Artvein, Animal Concerts, Defy Trends and Crypto.com NFT.

Cointelegraph

CointelegraphBTC’s sell-off is easing slightly, but traders are afraid that negative newsflow and future U.S. interest rate hikes could push the price lower.

Cointelegraphearn it

链向资讯

链向资讯BTC price could be poised for a big bounce despite Minerd’s prediction that price will drop to $8,000.

CointelegraphWhat is the essence of X to Earn? Does everything really need to Earn?

链向资讯Does it look like the move-to-earn games are the next big thing in the gaming sector? Genopets and Dustland Runner, STEPN and others are making moves to make it happen.

Cointelegraph