Elon Musk Reveals New Premium Tiers for X

Elon Musk made an announcement regarding the plans of X, formerly known as Twitter. Musk confirmed the impending launch of two distinct premium tiers, affirming prior reports and code discoveries.

Joy

Joy

Author: Bitget Wallet

In the global asset landscape, equity in unlisted companies—especially high-growth unicorn companies—is an asset sector that combines both scale and potential. However, for a long time, this growth potential has been almost entirely monopolized by professional institutions such as private equity (PE) and venture capital (VC), with only a few institutions and high-net-worth investors able to participate. Ordinary investors often can only watch the growth stories of unicorns in the news.

Blockchain and tokenization are changing this situation. By issuing tokens on-chain to represent equity in unlisted companies or their economic rights, the market hopes to build a new secondary market that can be traded 24/7 within a compliant framework, improving liquidity, lowering barriers to entry, and connecting TradFi and DeFi on a larger scale.

Institutions have also given this field extremely high expectations. For example, Citigroup believes that private equity tokenization could grow 80 times within ten years, approaching $4 trillion in size. Against this backdrop, the tokenization of equity in non-listed companies has naturally become one of the most watched sub-sectors in RWA. Its significance lies not only in technological innovation, but also in profound changes to asset participation mechanisms, exit methods, and profit structures. Bitget Wallet Research will take you through how equity tokenization will help non-listed companies break through this barrier in this article. II. A Trillion-Dollar "Siege": High Value, But Difficult to Enter and Exit From the asset side, equity in non-listed companies covers everything from startups to large private groups. Holders include founding teams, employee ESOPs/RSUs, angel investors, VC/PE funds, and some long-term institutions. From a funding perspective, according to publicly available data, global PE (private equity) assets under management are approaching $6 trillion, and VC (venture capital) assets under management are approximately $3 trillion, totaling about $8.9 trillion. Meanwhile, as of mid-2025, the total valuation of global unicorn companies hovered between $4.8 and $5.6 trillion, and this only represents the top few thousand companies at the very top of the pyramid; tens of thousands of mature private companies that haven't yet reached the "unicorn threshold" are not fully accounted for. Putting these figures together reveals a stark picture: a massive pool of assets worth trillions, yet a illiquid, walled city. On one hand, this market is inaccessible to the vast majority of people. Major jurisdictions generally limit primary private equity opportunities to a small circle of qualified and institutional investors, with minimum investment amounts often starting from hundreds of thousands or even millions of dollars. The combination of wealth and institutional barriers makes this asset class virtually untouchable for ordinary investors. On the other hand, those already inside the city often find it difficult to leave. For employees, angel investors, and VC/PE holders, the mainstream exit paths are almost exclusively IPO or M&A. Unicorn companies generally postpone their IPOs, with ten-year lock-up periods becoming the norm, making it difficult to realize paper wealth in the long term. While off-chain private equity secondary markets exist, they heavily rely on intermediaries, resulting in opaque processes, high costs, and long cycles, making them difficult to serve as large-scale liquidity outlets. The asymmetry between high-value assets and inefficient liquidity mechanisms provides a clear entry point for the tokenization of equity in non-listed companies—namely, reconstructing a new participation and exit path without disrupting regulatory and corporate governance order. III. What Does Tokenization Really Change? Under compliant conditions, the value of tokenization lies not only in moving equity onto the blockchain but also in reshaping three core mechanisms. First, continuous secondary liquidity. By tokenizing and splitting, high-value equity can be divided into smaller shares, allowing more compliant investors to participate in targets that were originally only for PE/VC with lower amounts. From the perspective of external investors, this is the starting point for ordinary people to buy some OpenAI/SpaceX; from the perspective of internal holders, it provides employees, early shareholders, and some LPs with a supplementary outlet besides IPO/M&A, enabling phased monetization in a 24/7 on-chain market under controllable thresholds. Secondly, it enables more continuous price discovery and market capitalization management. Traditional valuation of unlisted equity is highly dependent on financing rounds, with prices being discrete and lagging, even considered intermittent quotations. If, within a compliant framework, a portion of equity or economic rights is tokenized and put into continuous trading, the target company and primary investors can use more frequent market price signals to price subsequent financing, proactively managing market capitalization in a "quasi-public market" and bridging the valuation gap between primary and secondary markets. Finally, it provides new financing channels. For some high-growth companies, tokenization is not only a tool for transferring existing equity, but also a tool for issuing new capital. Through security token offerings (STOs) and other pathways, companies can potentially bypass expensive underwriting and lengthy IPO processes, directly raising funds from compliant global investors. This path is realistically attractive to companies that do not have short-term listing plans but wish to optimize their capital structure and improve employee mobility.

Regarding the topic of tokenization of equity in non-listed companies, there are currently roughly three implementation paths in the market, which differ fundamentally in their legal attributes, investor rights, and compliance paths.

The first type is the native collaborative model of real equity on-chain. In this model, the target company actively authorizes and participates, and equity registration, token issuance, and shareholder register maintenance are all completed within the regulatory framework.

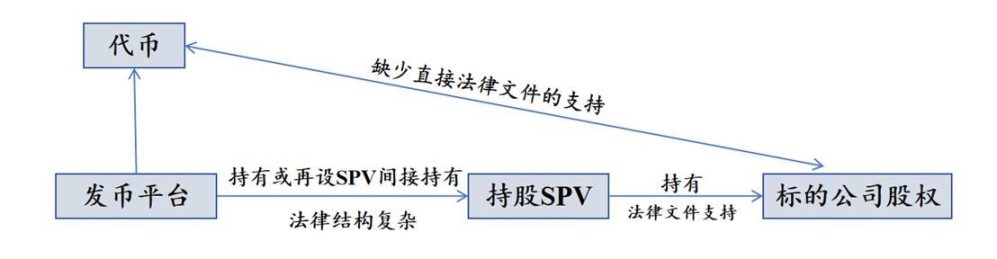

On-chain tokens are legally equivalent to equity, granting holders full shareholder rights such as voting rights and dividend rights. A prime example is Securitize, which helped companies like Exodus and Curzio Research tokenize their equity, trade it on the ATS platform, and even list it on the NYSE. Its advantages lie in clear compliance and well-defined rights, but this requires strong cooperation from the issuer, resulting in a relatively slow implementation pace. The second type is synthetic mirror-image derivatives. These projects do not hold real equity; instead, they "index" the valuation of the target company through contracts/notes, then issue perpetual contracts or debt-type tokens. Investors legally form a debt or contractual relationship with the platform and are not registered as shareholders of the target company; their returns depend entirely on contract settlement. Ventuals is a representative of this model, leveraging Hyperliquid's perpetual contract infrastructure to break down the valuations of non-listed companies like OpenAI into tradable valuation units, allowing users to go long or short. The third type is the most common SPV indirect holding model in the current Crypto landscape. The issuing platform first establishes a special purpose vehicle (SPV), which acquires a small amount of equity in the target company in the traditional private secondary market. Then, the SPV's beneficial rights are tokenized and sold externally. Investors hold contractual economic beneficial rights to the SPV, not direct rights listed on the target company's shareholder register. The advantage of this model is its practicality; it can connect real equity with on-chain capital to some extent even without the issuer's cooperation. However, it also naturally faces dual pressure from regulatory agencies and the target company's legal department. Transfer restrictions in the shareholder agreement, the SPV's lack of transparency, and liquidation arrangements may all become points of contention in the future.

Recently, a new signal is reshaping the market's perception of Pre-IPO RWA: what many users actually want is not shareholder status, but the ability to bet on the rise and fall of unicorns like OpenAI and SpaceX at any time.

Hyperliquid has amplified this demand to the extreme.

Through the HIP-3 programmable perpetual contract layer, any team can create a new perp market by staking enough HYPE. To reduce the pressure of a cold start, Hyperliquid also launched Growth Mode, providing new markets with approximately 90% of taker fees waived, allowing long-tail assets to quickly accumulate depth and activity in the early stages. Just last week, Hyperliquid directly launched the OPENAI-USDH trading pair. This means that a company that is not yet listed and whose valuation is entirely dominated by the private market has been brought into a 24/7, leveraged, globally accessible on-chain market, creating a significant disruption to the pre-IPO RWA. The anticipated impact is very obvious. Pre-IPO equity tokens, lacking liquidity, are marginalized by the depth and speed of the perp market before they can truly mature. If this trend continues, the primary market may even have to refer to the on-chain price of the perp market for valuation, which will completely change the price discovery logic of private assets. Of course, the question arises: what exactly is the price of OPENAI-USDH anchored to? The market capitalization of unlisted companies doesn't have continuous off-chain pricing, but the on-chain perpetual contracts operate 24/7. This likely relies on a "soft anchoring" system built from oracles, long-term valuation expectations, funding rates, and market sentiment. For the Pre-IPO RWA sector, there are two real-world challenges: First, there's the squeeze on the demand side. When ordinary investors only want to bet on price and don't care about shareholder rights, dividends, or voting rights, perpetual contract DEXs based on Hyperliquid are often simpler, more liquid, and offer more leverage tools. In contrast, Pre-IPO equity tokenization products, if they only offer price exposure, will find it difficult to compete with perp DEXs in terms of user experience and efficiency. Second, there's the contrast between narrative and regulatory logic. Equity tokenization requires repeated adjustments and collaborations with regulatory agencies like the SEC and the issuer's legal system; while perp DEXs, currently operating in a regulatory gray area, have captured mindshare and trading volume with their lighter contract structure and global accessibility. For ordinary users, "first invest in perpetual contracts, then consider whether there is real equity" is becoming a more natural path. This doesn't mean the Pre-IPO RWA narrative is invalid, but it serves as a wake-up call. If this sector wants to go further, it must find its own differentiated positioning among "real shareholder rights, long-term capital allocation, cash flow distribution" and "on-chain native liquidity." VI. Conclusion: The Rewriting of Asset and Market Structures is Beginning. The importance of tokenizing equity in non-listed companies lies not in allowing more people to buy a piece of a unicorn, but in addressing the most fundamental pain points of private equity: high barriers to entry, narrow exit paths, and lagging price discovery. Tokenization has shown for the first time that these structural constraints can be redefined. In this process, Pre-IPO RWA is both an opportunity and a stress test. On the one hand, it reveals real needs—employees, early shareholders, and investors are all seeking more flexible ways to transfer assets; on the other hand, it also exposes real constraints such as regulatory friction, price anchoring, and insufficient market depth. Especially under the disruptive impact of perp DEX, the industry has more directly witnessed the speed and power of native on-chain liquidity. However, this does not mean that tokenization will stagnate. Changes in asset structure, transaction structure, and market structure often do not depend on a single model winning, but rather on issuers and infrastructure finding a sustainable compromise between regulation and efficiency. A hybrid path is more likely to emerge in the future, preserving shareholder rights and governance structures within a compliant framework while also ensuring continuous liquidity and global accessibility of the on-chain market. As more assets are listed on-chain in composable and tradable forms, the boundaries of unlisted equity will be redefined: it will no longer be a scarce asset in a closed market, but a liquid node in a global capital network.

Elon Musk made an announcement regarding the plans of X, formerly known as Twitter. Musk confirmed the impending launch of two distinct premium tiers, affirming prior reports and code discoveries.

JoyThe practice of burning tokens has been a consistent strategy for Huobi since 2018, and as of October 15, 2023, a cumulative total of 301,002,441 HT has been burned.

Jasper

JasperSolana surged by 10% and breached the key resistance at $25, currently trading at $25.96, possibly heading for a 20% rise to reach $30.

Jixu

JixuFinland's progressive push in pioneering digital Euro and redefining the European monetary landscape.

Hui Xin

Hui XinThe emergence of quantum computing has raised concerns within the blockchain community regarding the security of existing systems, but Vitalik believes that a viable solution has been found.

Kikyo

KikyoThe Open Network Foundation (TON Foundation) has teamed up with Blockchain.com to provide seamless access to cryptocurrencies for Telegram's vast user base, which comprises over 700 million monthly active users.

JasperAlibaba and Tencent push forward AI investment in Zhipu, shaping China's tech landscape.

Hui XinBlockchain data analytics firm Santiment has sounded the alarm on the Ethereum (ETH) landscape, revealing a pronounced surge in accumulation by crypto whales.

JasperThe freeze order takes the form of "soulbound" NFTs and is firmly linked to the specific wallets under scrutiny.

Catherine

CatherineNavigating the future of healthcare by integrating AI's transformative role in medicine.

Hui Xin