AB DAO 官方 Twitter 账号升级,提醒社区注意风险

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

Alex

Alex

After the collapse of Luna-UST, stablecoins bid farewell to the era of stablecoins. CDP mechanisms (DAI, GHO, crvUSD) briefly became the community's hope. However, it was Ethena and the yield-pegging paradigm it represented that ultimately broke through the siege of USDT/USDC. This approach not only avoids the capital inefficiency caused by over-collateralization but also opens up the DeFi market with its native yield characteristics.

In contrast, after opening up the DEX market through stablecoin trading, the Curve ecosystem has gradually entered the lending market with Llama Lend and the stablecoin market with crvUSD. However, under the sway of the Aave ecosystem, crvUSD's issuance has long hovered around $100 million, essentially becoming a background figure. However, after the Ethena/Aave/Pendle flywheel was launched, Curve's new project Yield Basis also wanted to share a piece of the stablecoin market. It also started with revolving leveraged lending, but this time it is trading, hoping to use trading to eliminate the chronic disease of AMM DEX - impermanent loss (IL). Unilateralism eliminates impermanent loss. Curve's latest masterpiece, now your BTC is mine, hold your YB and stand guard. Yield Basis represents a renaissance. In one project, you can see liquidity mining, pre-mining, Curve Wars, staking, veToken, LP Token, and revolving loans. It can be said to be the culmination of DeFi development. Curve founder Michael Egorov was an early beneficiary of the development of DEX. He improved on Uniswap's classic AMM algorithm, x*y=k, and launched the stableswap and cryptoswap algorithms to support more "stablecoin transactions" and more efficient general algorithms. Large-scale stablecoin transactions established Curve as a key player in the on-chain "borrowing" market for early stablecoins like USDC/USDT/DAI. Curve also became the most important on-chain stablecoin infrastructure in the pre-Pendle era. Even the collapse of UST stemmed directly from the withdrawal of Curve's liquidity. In terms of token economics, the veToken model and the subsequent "bribe" mechanism, Convex, made veCRV a truly practical asset. However, after a four-year lock-up period, the pain felt by most $CRV holders is unspeakable. After the rise of Pendle and Ethena, Curve's market position was undermined. The core issue was that for USDe, hedging came from CEX contracts, which diverted traffic to sUSDe to capture returns, making stablecoin trading itself less important. Curve's initial counterattack came from Resupply, which launched in 2024 in collaboration with two established giants, Convex and Yearn Fi. Unsurprisingly, it collapsed, marking the failure of Curve's initial attempt. While Resupply wasn't an official Curve project, the consequences were significant. If Curve didn't fight back, it would be difficult to secure a ticket to the future in the new era of stablecoins. The expert's move is indeed unique. Yield Basis targets not stablecoins or the lending market, but the problem of uncompensated losses in AMM DEXs. However, a disclaimer: The real purpose of Yield Basis has never been to eliminate uncompensated losses, but to promote a surge in the issuance of crvUSD. But starting from the mechanism of uncompensated losses, LPs (liquidity providers) replace traditional market makers and, incentivized by a share of transaction fees, provide "bilateral liquidity" for AMM DEX trading pairs. For example, in the BTC/crvUSD trading pair, LPs need to provide 1 BTC and 1 crvUSD (assuming 1BTC = 1USD), and the total value of LPs at this time is 2 USD.

Correspondingly, the price p of 1 BTC can also be expressed as y/x. We agree that p=y/x. At this time, if the BTC price changes, for example, it rises 100% to $2, arbitrage will occur:

Pool A: The arbitrageur will use $1 to buy 1 BTC. At this time, the LP needs to sell BTC to get $2.

Pool B: Selling in Pool B when the value reaches $2, the arbitrageur makes a net profit of 2-1=$1.

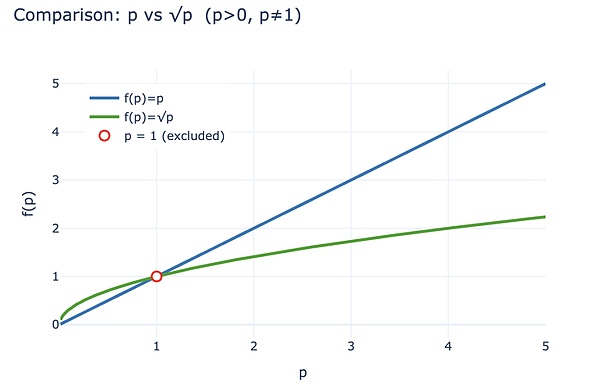

The arbitrageur's profit is essentially the profit of the LP in Pool A. To quantify this loss, we can first calculate the value of the LP after the arbitrage occurs: LP(p) = 2√p (x and y are both represented by p). However, if the LP simply holds 1 BTC and 1 crvUSD, it is assumed that they have no loss, which can be expressed as LP~hold~(p) = p + 1. According to the inequality, when p > 0 and not 1, 2√p < p + 1 is always obtained. Arbitrageurs' income essentially comes from LP losses. Therefore, driven by economic interests, LPs tend to withdraw liquidity and hold cryptocurrency. AMM protocols must retain LPs through higher fee sharing and token incentives. This is the fundamental reason why CEXs can maintain their advantage over DEXs in the spot market.

Image Caption: Uncompensated Loss

Image Source: @yieldbasis

From the perspective of the entire on-chain economic system, uncompensated loss can be regarded as a kind of "expectation". Once LP chooses to provide liquidity, it can no longer claim to obtain the income from holdings. Therefore, in essence, uncompensated loss is more of an "accounting"-style bookkeeping loss, and should not be regarded as a real economic loss. Compared with holding BTC, LP can also obtain transaction fees.

Yield Basis doesn't think so. They don't eliminate LP's expected losses by increasing liquidity or raising the fee ratio, but start from "market-making efficiency". As mentioned earlier, compared to the p+1 held, LP's 2√p will never outperform. However, from the perspective of the output ratio of 1 US dollar investment, the initial investment is 2 US dollars, and the current price is 2√p US dollars. The "yield" of each dollar is 2√p/2 = √p. Remember that p is the price of 1 BTC, so if you simply hold, then p is your asset return rate.

Assuming an initial investment of $2, after a 100% increase, the LP returns change as follows:

• Absolute increase: 2 USD = 1 BTC (1 USD) + 1 crvUSD -> 2√2 USD (arbitrageurs will take the difference)

• Relative rate of return: 2 USD = 1 BTC (1 USD) + 1 crvUSD -> √2 USD

Yield Basis Starting from the perspective of asset return, changing √p to p can ensure LP It is very simple to retain holding income while charging transaction fees. √p² is enough. From a financial perspective, it means 2x leverage, and it must be a fixed 2x leverage. Too high or too low will cause the economic system to collapse.

Image Caption: Comparison of LP Value Scaling of p and √p

Image Source: @zuoyeweb3

That is, allowing 1 BTC to achieve twice its own market-making efficiency, there is naturally no corresponding crvUSD participating in the fee sharing. BTC only has itself to participate in the yield comparison, that is, transforming from √p to p itself. Believe it or not, Yield Basis officially announced in February that it had raised $5 million, indicating that some VCs believed it. But! LP must add liquidity to the corresponding BTC/crvUSD trading pair. If the pool is full of BTC, it will not work. Llama Lend and crvUSD follow the trend and launch a double lending mechanism: 1. The user deposits 500 BTC (cbBTC/tBTC/wBTC), and YB (Yield Basis) uses 500 BTC to lend out 500 crvUSD of equivalent value. Note that it is equal at this time, using the flash loan mechanism, not a full CDP (originally about 200% pledge rate) 2. YB deposits 500BTC/500 crvUSD into Curve's corresponding BTC/crvUSD trading pool and mints it as $ybBTC 3. YB uses LP shares worth 1000U as collateral and goes to Llama Lend to use the CDP mechanism to borrow 500 crvUSD and repay the initial equivalent loan. 4. The user receives ybBTC representing 1000U, Llama Lend obtains the collateral of 1000U and eliminates the first equivalent loan, and the Curve pool obtains 500BTC/500 crvUSD liquidity. Ultimately, the 500 BTC "eliminated" its own loan and also received an LP share of 1,000 U, achieving a 2x leverage effect. However, please note that the equivalent loan was lent by YB, acting as the most critical middleman. Essentially, YB assumed the remaining 500U loan share from Llama Lend, so YB also received a share of Curve's handling fees.

If users think that 500U of BTC can generate 1000U of transaction fee profit, then they are right, but if they think that all of it should be given to themselves, that would be a bit rude. In short, it is more than a 50-50 split. YB's little idea is to pay pixel-level tribute to Curve.

Let's calculate the original profit:

Among them, 2x Fee means that a user investing 500U of BTC equivalent can generate 1000U of transaction fee profit, Borrow_APR represents the Llama_Lend rate, and Rebalance_Fee represents the fee for arbitrageurs to maintain 2x leverage, which is essentially still paid by LP.

Now there is a good news and a bad news:

• Good news: All the lending income of Llama Lend goes back to the Curve pool, which is equivalent to passively increasing the LP income

• Bad news: The Curve pool’s transaction fees are fixed at 50% to the pool itself, that is, LP and YB must share the remaining 50% of the transaction fees

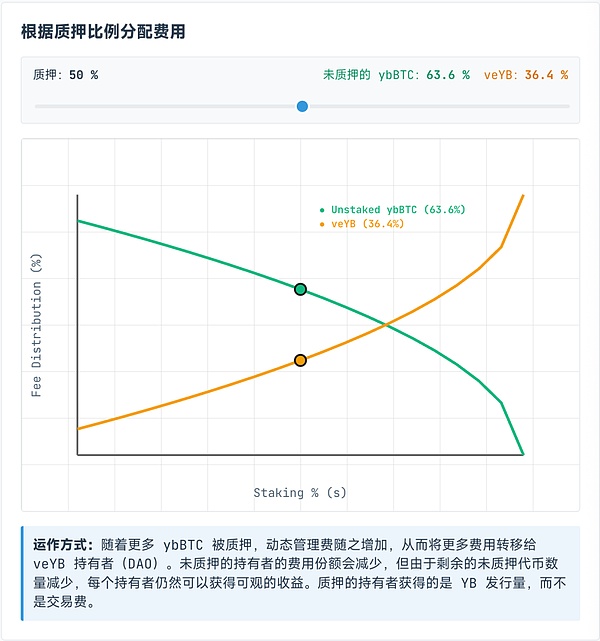

However, the transaction fees allocated to veYB are dynamic. In fact, they are dynamically divided among ybBTC and veYB holders, of which veYB is fixed at a minimum of 10%. The guaranteed profit margin means that even if no one stakes ybBTC, they will only receive 45% of the original total revenue, while veYB, or YB itself, will receive 5% of the total revenue. A surprising result: even if no one stakes ybBTC to YB, they will only receive 45% of the transaction fees. If you choose to stake ybBTC, you will receive YB tokens, but you will forgo the transaction fees. If you want both, you can continue to stake YB and exchange it for veYB, which will earn you the transaction fees.

Image description: ybBTC and veYB revenue sharing

Image source: @yieldbasis

Uncompensated losses will never disappear, they will just be transferred. You might think you're using 500U worth of BTC to achieve the market-making effect of 1000U, but YB doesn't guarantee you all the market-making profits. Furthermore, after staking veYB, you need to unstake it twice, converting veYB to YB and ybBTC to wBTC, to get your original funds and profits back. However, if you want to gain full voting rights on veYB, which is a bribery mechanism, then congratulations! You've secured a four-year lock-up period. Otherwise, your voting rights and profits will gradually decrease over the staking period. So, whether the four-year lock-up and the sacrifice of BTC liquidity for YB are worth it depends on your personal considerations. As mentioned earlier, uncompensated losses are bookkeeping losses. As long as liquidity isn't withdrawn, they remain floating losses. YB's current elimination plan is essentially "bookkeeping income," giving you a floating profit anchored to your holdings, thereby fostering its own economic system. You want to leverage 500U to generate 1000U in transaction fees. YB wants to "lock up" your BTC and sell you its own YB. Multi-party negotiations embrace the growth flywheel. In this era of great returns, come if you have a dream. Based on Curve and using crvUSD, while it will empower $CRV, it also launches the Yield Basis protocol and its token, $YB. So, will YB maintain its value and increase in value four years from now? I'm afraid... Beyond the complex economics of Yield Basis, the key is crvUSD's market expansion. Llama Lend is essentially part of Curve, but Curve's founder is proposing to issue an additional $60 million in crvUSD to provide initial liquidity for YB. That's a bit bold.

YB will give benefits to Curve and $veCRV holders as planned, but the core is the pricing and appreciation of YB Token. After all, crvUSD is U, so is YB really a value-added asset?

Not to mention another ReSupply incident, which would affect Curve itself.

Therefore, this article does not analyze the token linkage and profit-sharing plan between YB and Curve. $CRV is a lesson learned not far away, and $YB is destined to be worthless, so there is no point in wasting bytes.

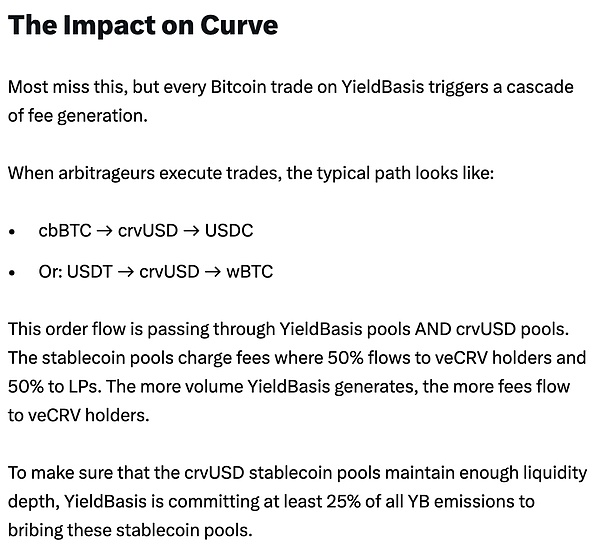

However, in his defense of his issuance, we can get a glimpse of Michael's ingenious ideas. The BTC deposited by users will "increase" the equivalent value of crvUSD. The benefit is that the supply of crvUSD will be increased, and each crvUSD will be put into the pool to earn transaction fees. This is a real trading scenario. But in essence, this portion of the crvUSD reserve is equal, not in excess. If increasing the reserve ratio isn't an option, then increasing crvUSD's profitability is another approach. Remember the relative rate of return? According to Michael's vision, loaned crvUSD will effectively collaborate with existing trading pools. For example, wBTC/crvUSD will be linked to crvUSD/USDC, boosting the former's trading volume and, in turn, the latter's. The transaction fees from the crvUSD/USDC pair will be split 50% among $veCRV holders, with the remaining 50% going to limited partners. This is arguably a very dangerous assumption. The crvUSD lent to YB by Llama Lend, as mentioned above, is exclusively used in a single pool. However, pools like crvUSD/USDC are not accessible. At this point, crvUSD is essentially under-reserved. Once the currency fluctuates, it's easily exploited by arbitrageurs, leading to the familiar death spiral. Problems with crvUSD would impact YB and Llama Lend, ultimately impacting the entire Curve ecosystem. It's important to note that crvUSD and YB are tightly coupled. 50% of newly issued liquidity must enter the YB ecosystem. The crvUSD used by YB is segregated in issuance, but not in usage. This presents the biggest potential risk factor.

Image Description: Curve Profit Sharing Plan

Image Source: @newmichwill

Michael's plan is to use 25% of the issuance of YB Token to bribe the stablecoin pool to maintain depth. This is almost a joke. Asset security: BTC>crvUSD>CRV>YB. When the crisis comes, YB can't even protect itself, so what can it protect? YB's own issuance is a profit-sharing product of the transaction fees of the crvUSD/BTC trading pair. Remember, the same is true for Luna-UST. UST is minted with the equivalent value of Luna's burn volume, and the two are mutually dependent. The same is true for YB Token <>crvUSD. It can be even more similar. According to Michael's calculations, based on the BTC/USD trading volume and price performance over the past six years, he calculated that he can guarantee a 20% APR and a 10% return even in a bear market. The peak of the bull market in 2021 could reach 60%. If crvUSD and scrvUSD are empowered a little bit, surpassing USDe and sUSDe is not a dream. Due to the sheer volume of data, I haven't backtested to verify its calculations. But don't forget, UST also guaranteed a 20% return, and the Anchor + Abracadabra model ran for quite some time. Wouldn't the YB + Curve + crvUSD combination be any different? At least, UST frantically purchased BTC as a reserve before the collapse, while YB leverages its reserve directly with BTC, which is a huge improvement. To forget is to betray. Starting with Ethena, on-chain projects have begun to pursue real returns, rather than simply focusing on price-to-dream ratios. Ethena utilizes CEX to hedge ETH for yield capture, distributes revenue through sUSDe, and employs the $ENA treasury strategy to maintain the trust of major investors and institutions. These multiple maneuvers are crucial to maintaining the USDe's tens of billions in circulation. YB's pursuit of real trading returns is not inherently problematic, but arbitrage differs from lending in that transactions are more immediate. Each crvUSD is a joint liability of YB and Curve, and the collateral itself is borrowed from users, leaving the company's own capital close to zero. crvUSD's current issuance is small, making it easy to maintain a growth flywheel and a 20% return rate in the early stages. However, once scale expands, YB price increases, BTC price fluctuations, and crvUSD's declining value capture will all lead to significant selling pressure. The US dollar is an unanchored currency, and crvUSD will soon be one as well. However, the embedded risks of DeFi have already been priced into the overall systemic risk of the chain, so if it is a risk for everyone, it is not a risk at all. Instead, those who do not participate will passively share the losses of the collapse. Conclusion The world will give a person an opportunity to shine, and those who can seize it are heroes.

The Yield Basis of traditional finance is the U.S. Treasury yield. Will the Yield Basis on the chain be BTC/crvUSD?

The YB logic can only be established if the on-chain transactions are large enough, especially since Curve itself has a huge trading volume. In this case, it makes sense to eliminate uncompensated losses. You can make an analogy:

• The amount of electricity generated is equal to the amount of electricity consumed. There is no static "electricity". It is used as soon as it is generated

• The trading volume is equal to the market value. Every token is flowing and can be bought and sold at the same time

Only through continuous and sufficient transactions can the price of BTC be discovered, the value logic of crvUSD be closed, additional issuance can be made from BTC lending, and profits can be made from BTC transactions. I am confident in the long-term rise of BTC. BTC is the CMB (Cosmic Microwave Background) of the crypto universe. Since the financial crash of 2008, as long as humanity doesn't want to reset the world order through revolution or nuclear war, BTC's overall trend has been upward. This isn't due to a growing consensus on BTC's value, but rather confidence in the inflation of the US dollar and all fiat currencies. However, I have moderate confidence in the Curve team's technical capabilities, and after ReSupply, I have deep doubts about their ethics. However, it's unlikely that another team would dare to attempt this. Unfortunately, the money is lost, and those who were destined to succeed suffer uncompensated losses. UST frantically bought BTC on the eve of its demise, switching to USDC during fluctuations in USDE reserves. Sky has even more enthusiastically embraced Treasury bonds. Good luck to Yield Basis this time around.

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

AlexArweave, Arweave's working principle and significance of existence Golden Finance, this article briefly introduces Arweave's working principle and value.

JinseFinance

JinseFinanceThe U.S. economy declined more than expected, global liquidity tightened more than expected, domestic industrial policies were not implemented as expected, the "black swan" event before the U.S. election had an impact, and expectations of global geopolitical turmoil rose more than expected.

JinseFinanceThe S&P 500 (an index of the top 500 US companies) is still below its mid-July peak and the level at the end of July when the “crash” began. What is causing this downward trend? Does it portend more serious problems for the US economy?

JinseFinanceOn August 8, the U.S. Federal Reserve took a major enforcement action against Pennsylvania-based Customers Bank, marking the U.S. government’s gradual increase in regulatory oversight of cryptocurrency-related businesses.

JinseFinanceGolden Finance launches the 2190th issue of the cryptocurrency and blockchain industry morning report "Golden Morning 8:00" to provide you with the latest and fastest digital currency and blockchain industry news.

JinseFinanceJinseFinanceJinseFinanceThe Ethereum Foundation's Danny Ryan discusses how the Merge will increase security and explains how proof of stake impacts developers.

Future

FutureNigel Dobson, head of portfolio banking services at ANZ, said: "When we looked at this in depth, we came to the conclusion that this is a significant protocol shift in financial market infrastructure."

Cointelegraph

Cointelegraph