Hyperliquid Technical Interpretation: HyperEVM and Its Potential Problems

A technical interpretation of the cross-chain bridge contract structure and HyperEVM's dual-chain interaction implementation mechanism.

JinseFinance

JinseFinance

Author: Jia Huan, ChainCatcher

On September 5th, Hyperliquid announced in its Discord group that it would issue its native stablecoin, USDH, and announced an 80% fee reduction for spot trading pairs.

Several institutions subsequently bid to become issuers of USDH, including Sky (formerly MakerDAO), Ethena, Frax, Agora, and Native Markets. Circle's CEO, directly harmed by this move, responded by saying, "Don't believe the hype."

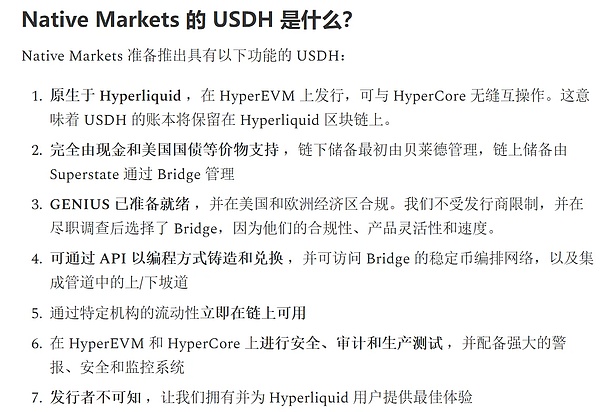

However, as of September 15th, Hyperliquid's native token, HYPE, continued to break new highs, reaching $53.64. According to CoinGecko data, its price has risen by 7.77% over the past seven days. The Native Markets team has won the Hyperliquid USDH stablecoin bidding and plans to enter the testing phase "within a few days." USDH issuance: An expected closed-loop ecosystem strategy. Hyperliquid was once considered one of the most successful projects of this cycle. With a team of just 11 people, each employee generates over $100 million in annual revenue and holds over 75% of the decentralized contract market. According to Defilama data, Hyperliquid's revenue reached $106 million in August 2025, including nearly $400 billion in perpetual contract trading volume. Despite being a veritable industry giant, Hyperliquid suffers from a fatal weakness. Its USD liquidity relies on USDC, a centralized, external stablecoin that can be frozen at any time. Meanwhile, Hyperliquid holds nearly $5.7 billion in USDC deposits. This means that annually (at a 4% interest rate), over $220 million in interest income goes to external stablecoin issuers rather than the ecosystem itself. Therefore, both from the perspective of the platform's philosophy and its profitability, Hyperliquid must issue its own native stablecoin. Validator Voting: Decentralization or "Pulling the Cord"? Hyperliquid's USDH issuance differs from that of centralized companies like Circle or Tether, where the reserve funds are controlled by the company and interest income accrues to it. USDH issuance, however, is governed by a community-driven on-chain voting mechanism. Revenue generated by USDH will be redirected back to the Hyperliquid ecosystem, used to repurchase tokens or provide funds to support ecosystem development. This decentralized decision is theoretically transparent, but critics argue that a vote dominated by 21 validators is highly centralized. In contrast, Ethereum has over 40,000 validators, providing a strong defense against collusion. Native Markets, founded by Max Fiege, an advisor to Hyperion (HYPE Digital Asset Treasury), has secured the rights to issue USDH. While Native Markets has no track record of issuing stablecoins, it distinguishes itself as the only team to have deployed and tested token liquidity on the Hyperliquid testnet and mainnet.

Image source: Native Markets proposal

However, the community has many controversies regarding this proposal, which mainly focus on three aspects.

● Dissatisfaction with existing protocols Max, the head of Hyperstable (an existing stablecoin protocol), protested that Hyperliquid had banned the USDH codename and forced it to use USH. Now reopening it is unfair to the team that has invested resources and built on USH. Max suggested that USDH continue to be banned or that it be developed internally by the Hyperliquid Foundation to maintain neutrality. ● Controversy surrounding the fairness of the Native Markets proposal: Some users questioned the fairness of the proposed deployment address, claiming it was a new wallet that received funds five hours before the USDH plan was announced, suggesting an undisclosed relationship with the Hyperliquid Foundation. Hyperstable's Max also considered the proposal overly detailed, suggesting he had prior insider knowledge. ● Potential conflicts of interest with Stripe: Native Markets' reliance on Stripe's Bridge platform has raised concerns. Agora CEO Nick van Eck warned that Stripe, as a vertically integrated competitor (involving wallets, infrastructure, and more), could lead to Hyperliquid losing its economic autonomy. Meanwhile, the $JELLY incident in March 2025 exposed Hyperliquid's governance risks. Faced with a malicious attack threatening network security, the team urgently delisted the token through a validator vote, a move that has also been criticized as a centralized "wire-pulling" operation. The Vision of "On-Chain Binance": More Than Just a DEX Hyperliquid addresses a series of issues currently faced by centralized exchanges, starting with no KYC, zero gas fees, and an on-chain order book, and gradually building its own L1 ecosystem. Image source: X user Pang Jiaozhu (@kiki520_eth) At the same time, Hyperliquid has also proposed its own HIP (Hyperliquid Improvement Proposals), similar to EIPs. HIP-1 defines native token standards, enabling projects to issue tokens on Hyperliquid and create on-chain order books, adding a spot market to Hyperliquid. HIP-2, modeled after UniSwap, provides a liquidity strategy for token trading, eliminating the need for projects to pay high market maker fees and thereby attracting more projects to issue tokens on Hyperliquid. HIP-3 allows users to stake 1 million HYPE tokens to deploy any type of contract market, including traditional stocks, funds, bonds, and more, laying the foundation for Hyperliquid's transformation from a single DEX to an open financial infrastructure provider. From its initial roots as a perpetual contract exchange, to its HIP-driven spot market and liquidity mechanism, and finally to the infusion of the USDH native stablecoin, Hyperliquid's ambition has always been more than just a DEX. So, will it become the next legend? The answer may lie in the next HIP proposal or the next price breakthrough of HYPE.

A technical interpretation of the cross-chain bridge contract structure and HyperEVM's dual-chain interaction implementation mechanism.

JinseFinanceSince the launch of HYPE, Hyperliquid has achieved tremendous growth in both trading volume and revenue.

JinseFinanceBuilding a cult around an image or slogan that has nothing to do with the underlying product is a replacement for the cult that should be around your product itself.

JinseFinance在DeFi投资者准备迎接HYPE代币发行之际,是什么让Hyperliquid吸引了这么多人的目光?

JinseFinanceThe most discussed topic today is why @HyperliquidX is more successful than other Perps. Let me talk about $HYPE from my personal experience.

JinseFinanceThe launch of Beam Chain has drawn sharp criticism from many prominent figures and community members in the blockchain space. However, such fierce criticism also shows that people still have high expectations for Ethereum.

JinseFinanceHyperliquid does not do any publicity, has never accepted any financing from venture capital (no performance pressure), and does not rely on subsidies to attract trading volume. With just strong products, they can surpass many competitors.

JinseFinanceProtocol 142 will solve Memecoin’s long-standing market challenges and lead it into a new era of greater prosperity and maturity.

JinseFinanceHyperliquid的生态系统正在迅速扩张,这得益于成功的现货代币发行和奖励积分计划。

Bernice

BerniceJoin the DragonEgg airdrop on Solana and be part of the monumental distribution of 60% of DGE tokens. Apply from January 31 to February 8 at degfinance.org and seize your chance to engage with a thriving crypto community. Don't miss this opportunity to be part of DragonEgg's journey on the Solana blockchain!

Brian

Brian