比特币回调至 66,500 美元,以太坊跌破 2,700 美元:市场健康调整还是趋势逆转?

比特币昨日触及 69,546 美元高点后回落,盘中最低跌至 66,500 美元,令部分投资者出局。以太坊跌幅更大,回到 2,640 美元的关键盘整区。市场在短期内面临健康调整或是深度回调,仍有待观察。

Alex

Alex

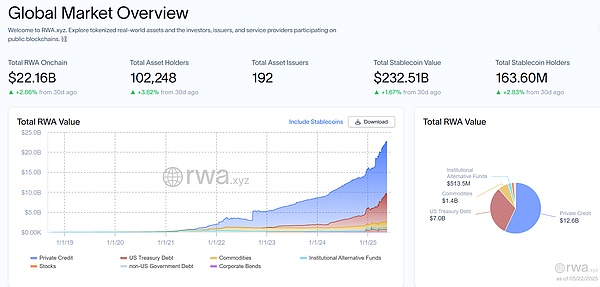

The global asset tokenization process is accelerating. According to data from the RWA.xyz platform, as of April 2025, the total value of RWA assets on the global chain has exceeded US$22 billion. At the same time, Deloitte also predicted in a research report that the scale of the tokenized real estate market will reach US$4 trillion in 2035.

In this wave of financial innovation, Hong Kong has rapidly developed into a pioneer in the compliance development of the RWA field with its unique institutional advantages - from the charging pile asset tokenization project launched by Longxin Group to the first compliant tokenized fund in Asia launched by China Asset Management. The successful implementation of multiple benchmark cases has confirmed the application potential of this innovative financing method in the field of physical assets.

What exactly is RWA?

Why choose RWA and what are its advantages?

How does Hong Kong regulate RWA?

What compliance points should mainland enterprises pay attention to when conducting RWA in Hong Kong?

The Crypto Salad team has been deeply involved in the cryptocurrency industry for many years and has rich experience in dealing with RWA project architecture design and related complex cross-border compliance issues. In this article, we will combine the team's latest RWA project experience and industry research results to sort out and answer the above questions from the perspective of professional lawyers.

(The above picture is the global on-chain RWA asset dashboard compiled by the website RWA.xyz)

RWA, the full name of which is "Real World Assets", is an innovative financial model based on blockchain technology. It uses blockchain technology to map physical assets or financial assets to the chain, thereby converting them into digital tokens with high liquidity and divisibility. This conversion process not only realizes the digital expression of assets, but also gives these real assets unprecedented transparency and traceability through blockchain technology.

Although we can explain the connotation and extension of the concept of RWA at the theoretical level, it is difficult for all parties to reach a complete consensus when it comes to specific project practices.

"What is a real RWA? Which projects should be identified as RWA projects" - professionals, regulators, and project parties all have their own perspectives and opinions on the above issues. The Crypto Salad team combined project experience and research results to give its own views from the perspective of legal compliance: "RWA is actually a broad concept, and there is no so-called standard answer. All processes that realize asset tokenization through blockchain technology can be called RWA." For an in-depth analysis of the concept of RWA, please see: "Web3 Lawyer Decryption: What kind of RWA do you understand?

(I) Activate heavy asset financing scenarios that are difficult to reach with traditional finance

First, taking real estate, infrastructure income rights, commodities and other assets as examples, these assets are difficult to finance through traditional financial instruments due to complex issues such as heavy asset attributes, liquidity restrictions and compliance supervision. The RWA model combines blockchain technology to divide the ownership of these physical assets or equity assets, convert them into highly liquid digital tokens, and raise investors' funds by issuing digital tokens. RWA has opened up a new financing method for the above assets, allowing these previously "sleeping" assets to be revitalized. This means that at a time when there are few financing channels, financing is difficult, and financing costs are high, RWA can provide companies with a new "blood-making method."

For investors, the divisibility of tokens lowers the investment threshold for specific assets. Taking real estate investment as an example, under the framework of traditional finance, investors who want to invest in real estate often need to spend millions of yuan to purchase the entire property. The high capital threshold excludes many small and medium-sized investors. Relying on the RWA model, investors may only need to spend $50 to purchase a token representing part of the property rights of real estate. By holding the token, investors will be able to enjoy the investment returns brought by the appreciation of real estate and rent.

(II) Reduce financing costs and improve financing efficiency

In the traditional securities issuance process, enterprises and projects need to go through a strict and lengthy review process, and the qualifications, scale, project operation methods, etc. of the issuer must meet high requirements. Taking the issuance of asset-backed securities (ABS) as an example, its supervision and approval standards are extremely strict, which to a large extent limits the financing needs of some enterprises.

Under the RWA model, in addition to complying with local compliance requirements, the financing party has relatively few other access requirements and restrictions, but it is still necessary to comply with the underlying assets. Therefore, this financing method circumvents the lengthy review process and cumbersome issuance procedures in the traditional financing process to a certain extent, and also effectively reduces financing costs.

(III) Customized Transaction Structure

RWA financing provides enterprises with unprecedented flexibility, enabling them to tailor financing structures according to market demand and their own development goals. Enterprises can independently design key terms such as profit distribution model, redemption mechanism, token unlocking mechanism, and adjust issuance conditions in real time according to market dynamics. This high degree of flexibility enables enterprises to accurately match investors' expectations and risk preferences, thereby improving the targeting and success rate of financing.

Fundamentally, in addition to introducing blockchain technology to improve financing efficiency and transparency, RWA has also changed the financing logic under the traditional financial framework. Traditional financing models, whether debt financing or equity financing, mostly rely on corporate credit as the basis. In contrast, RWA uses blockchain technology to effectively separate "corporate credit" from "asset credit". In this way, even if the credit status of the issuer is average, as long as the underlying assets are of high quality, financing can be obtained based on the credit of the assets themselves.

This feature is similar to the ABS model mentioned above. However, although the two have similarities in financing logic, the core difference between the two lies in the investor groups covered and the ecological effects they form.

The ABS market is mainly dominated by traditional financial institutions, the market participants are relatively limited, and most of the trading entities are institutional investors. This feature makes the overall trading depth of ABS insufficient, the market coverage is relatively narrow, and lacks a wide range of influence.

In contrast, the participants in the RWA market are more diverse. In addition to traditional financial institutions, the RWA financial market will also attract many crypto investors and industry ecological partners. Therefore, in the RWA market, from professional institutions to ordinary retail investors to partners, they can freely buy, sell and use the token and become an important part of the token ecology.

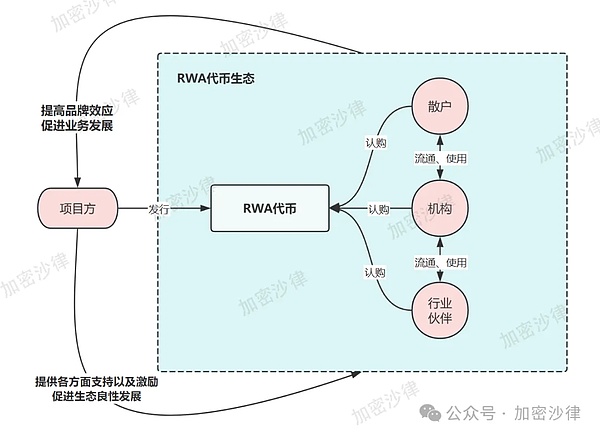

Many investors have formed a large and active ecology and community around the RWA token. The resulting strong community cohesion and ecological stickiness will provide strong support for the long-term value growth of RWA tokens, thereby promoting the healthy development of the market. The prosperity of the on-chain ecology can also feed back the development of the project's off-chain business and significantly improve the brand voice of the project.

And this on-chain-off-chain collaborative positive feedback development model is the real subtlety of the RWA model compared to traditional financing methods, and it is also difficult to achieve with the ABS model.

At present, the market is still constantly cultivating and expanding the RWA investor group. In the current RWA track, the leading ones are all kinds of financial asset tokenized products. Because financial assets themselves have the characteristics of high compliance, high degree of standardization, and low difficulty in data capture, the tokens of financial assets have unique advantages and demonstration effects in the RWA track.

The wave of tokenization of financial assets began with products such as U.S. Treasury bonds and money market funds with the lowest underlying asset risks. A typical example is the BUIDL tokenized investment fund launched by BlackRock, a top global asset management group. So far, the total market value of BUIDL has reached US$2.89 billion. In addition to low-risk financial assets, high-risk financial assets such as stocks and ETFs have also recently embarked on the fast track of tokenization. On May 22 and 23, Kraken Exchange and Ondo Finance announced that they would promote the tokenization and on-chain trading of financial assets such as stocks and ETFs.

With the rapid implementation and development of various tokenized financial assets and stablecoins, the investor scale and liquidity of the RWA market will reach a new height. In the future, more and more different types of RWA products will enter the field of vision of investors, thereby attracting more Web2 users and traditional financial investors to enter the RWA ecosystem. The flywheel of the entire RWA ecosystem will circulate and develop rapidly, bringing new wealth effects and industry opportunities.

(The above picture is a schematic diagram of the RWA ecological development model, for reference only)

(I) Regulatory principles

As the backbone of Hong Kong's market supervision, the Hong Kong Securities and Futures Commission has adopted the "See-Through Approach" in the process of supervising RWA products.The core of this principle is that the core focus of supervision is not whether the product adopts the form of "tokens", but focuses on the financial attributes of the real assets corresponding to the tokens. In short, Hong Kong's regulation of RWA is to return to the essence of the underlying assets, rather than sticking to the form of tokens. This regulatory principle is also a concrete manifestation of the concept of "same business, same risks, same rules".

(II) Specific regulatory documents

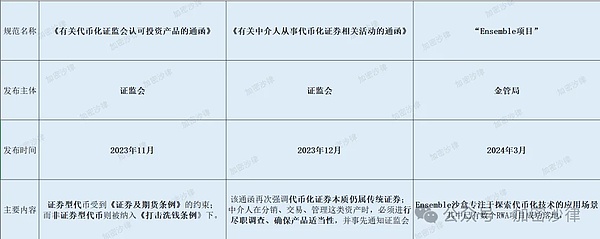

1. In November 2023, the Securities and Futures Commission (SFC) of Hong Kong issued the Circular on Tokenized SFC-approved Investment Products, which clarified the concept of layered supervision for the issuance of security tokens.

According to relevant regulations, Securities Tokens are subject to the Securities and Futures Ordinance and must meet the relevant requirements set forth by the SFC in the above circular, including token issuance qualifications, information disclosure, and investor suitability. Non-Securities Tokens are included in the regulatory scope of the Anti-Money Laundering Ordinance.

2. In November 2023, the Hong Kong Securities and Futures Commission issued the Circular on Intermediaries Engaged in Tokenized Securities-Related Activities.

The circular once again emphasized that although tokenized securities are issued using blockchain technology, they are still traditional securities in nature and must comply with current securities laws and regulations. At the same time, intermediaries must conduct due diligence, ensure product suitability, and notify the Securities and Futures Commission in advance when distributing, trading, and managing such assets.

3. In March 2024, the HKMA launched the "Ensemble Project".

Among them, the Ensemble sandbox focuses on exploring the application scenarios of tokenization technology, among which several RWA projects have been successfully implemented, covering multiple industries such as green bonds, carbon credits, real estate, and supply chain finance.

In general, from 2023 to 2024, the Hong Kong Securities and Futures Commission has successively issued a number of circulars and guidance documents involving tokenized investment products, further clarifying the specific regulatory standards for RWA products (especially tokenized securities), thereby providing clear regulatory guidance for the steady development of the RWA market.

(The above picture is a summary of the relevant regulatory framework for RWA)

The above article specifically analyzes Hong Kong's regulatory framework for RWA, and the complete and systematic review of Hong Kong's virtual asset regulatory policies can be found below: "Master in One Article: A Systematic Review of Hong Kong's Virtual Asset Regulatory Policy Framework"

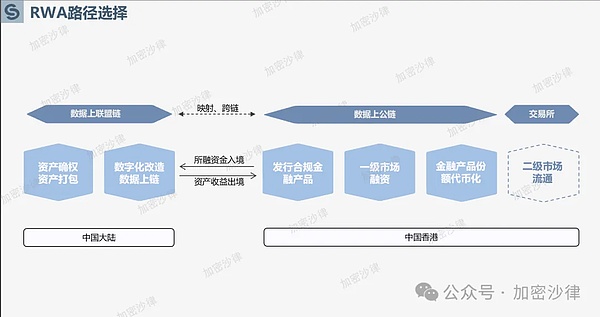

The reason why the issuance of RWA must be a cross-border structure is that in mainland China, token issuance is a regulatory red line that cannot be crossed. On September 4, 2017, the People's Bank of China and seven other departments issued the "Announcement on Preventing the Risks of Token Issuance and Financing", clarifying that no organization or individual may illegally engage in token issuance and financing activities, and all types of token issuance and financing activities should be stopped immediately.

Therefore, the issuance of RWA projects in mainland China must take place overseas. Among them, Hong Kong has become one of the best choices for the implementation of RWA projects by Chinese companies due to its perfect regulatory framework, friendly policy attitude and rich industry ecology. The following will analyze the key compliance points and framework design ideas for carrying out RWA projects in Hong Kong from the three levels of underlying assets, data on-chain and capital circulation.

(The above figure is a schematic diagram of the overall framework for issuing RWA in Hong Kong)

(I) Compliance of underlying assets

1. Confirmation of asset rights

Since the essence of RWA is the tokenization of real-world assets, the holders of the tokens will directly or indirectly own the specific ownership of real-world assets. Therefore, in order to ensure that the subsequent RWA tokens can be legally issued, circulated and redeemed, the underlying asset owner, that is, the RWA project party, must ensure that they have legal and clear ownership of the assets.

The RWA project compliance team needs to conduct detailed due diligence on the underlying assets during the project to ensure the legitimacy of the ownership. Specifically, the compliance team will conduct ownership dispute investigation during the due diligence process, collect and verify the ownership documents, public registration information, litigation, pledge, mortgage or judicial freeze of the underlying assets and other relevant information.

2. Asset Audit

After completing the asset confirmation, the project party also needs to hire a professional auditing agency to audit the underlying assets.

The audit report will provide reference data for subsequent asset pricing and issuance, including but not limited to the following elements:

Asset market value - Fair market value assessment by professional appraisers or valuation experts, referring to historical transaction data, market conditions and similar asset prices.

Asset depreciation and impairment- For fixed assets, consider the depreciation method, asset life and possible impairment to ensure that the assessed value reasonably reflects the actual value.

Asset risk identification- Identify risks associated with assets, such as market risk, legal risk, liquidity risk, operational risk, etc.

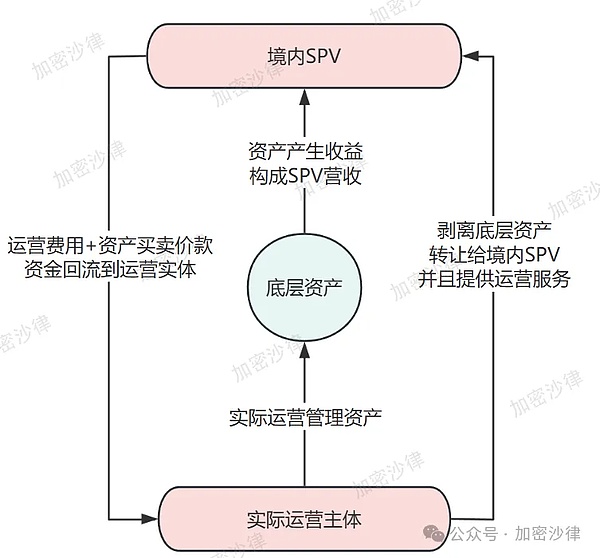

3. Asset divestiture

As mentioned above, the core value of RWA lies in directly financing based on the credit of high-quality assets, thereby breaking away from the traditional financing model based on corporate credit. Therefore, when carrying out RWA projects, it is necessary to divest the underlying assets from the actual operating entity of the project party, so as to achieve risk isolation between the operating entity and the underlying assets.

The following will combine the actual cases that the Crypto Salad team is promoting to illustrate one of the asset divestiture architecture designs:

First, the project compliance team will assist the project party in setting up an SPV (special purpose entity) in China.

Second, the actual operating entity transfers the underlying assets to the SPV through a buying and selling transaction.

Finally, the SPV will sign an operating service agreement with the project party, and the project party will be responsible for the operation and management of the underlying assets, and the SPV will pay the corresponding service fees to the project party on a regular basis.

(The above figure is a schematic diagram of the asset divestiture framework design, for reference only)

In summary, through this asset divestiture structure, the project party can transfer the ownership of the assets to the SPV company, achieve risk isolation and facilitate subsequent asset packaging and issuance. At the same time, although the actual operating entity no longer owns the ownership of the asset, it can continue to manage and operate the underlying assets through the service agreement.

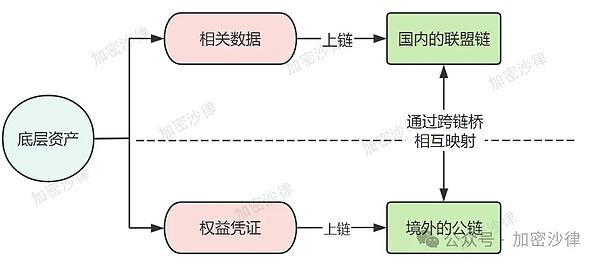

(II) Compliance with data on the chain

Due to my country's current strict supervision of cross-border data transmission and data exchange, most RWA projects will not choose to transfer relevant data overseas and circulate and disclose them on the public chain.

During the research process, the Crypto Salad team found that under the premise of meeting the compliance requirements of my country's Data Security Law and Personal Information Protection Law, the project party is more inclined to choose the "two chains and one bridge" model to realize data on the chain.

Specifically, RWA asset data chooses to be on the domestic alliance chain for data on-chain and completes the evidence storage, while the corresponding RWA pass is deployed on a high-performance public chain abroad. The RWA pass circulating overseas and the data on the domestic chain are mapped and bound through a cross-chain bridge.

Such an architectural design not only solves the problem of on-chain evidence storage of RWA underlying asset-related data, ensures the transparency and traceability of asset data, but also avoids the compliance red line of cross-border data transmission.

(The above picture is a schematic diagram of the "two chains and one bridge" model, for reference only)

In addition to the "two chains and one bridge" model, the RWA project can also rely on the Hainan Free Trade Port Cross-border Data Flow Pilot Zone (hereinafter referred to as the "Hainan Free Trade Data Port") to complete cross-border data chaining and circulation. According to the relevant information that has been disclosed, the Crypto Salad team concluded that the core framework of the current Hainan Free Trade Port data export plan is as follows: 1. The regulatory agency shall actively classify and grade the data; 2. Establish a data whitelist. If the data is included in the whitelist, it can be directly exported without approval; 3. If the data is not included in the whitelist, the regulatory agency will apply the corresponding regulatory procedures according to different data types: personal information protection certification, data export security assessment, and personal information export standard contract filing. In the actual process of promoting the project, the Crypto Salad team found that in addition to the compliance requirements of the data circulation link, there will also be some key compliance points and administrative supervision requirements in the data collection, storage, desensitization, and packaging of RWA underlying assets. Due to the length of this article, this article will not be discussed here.

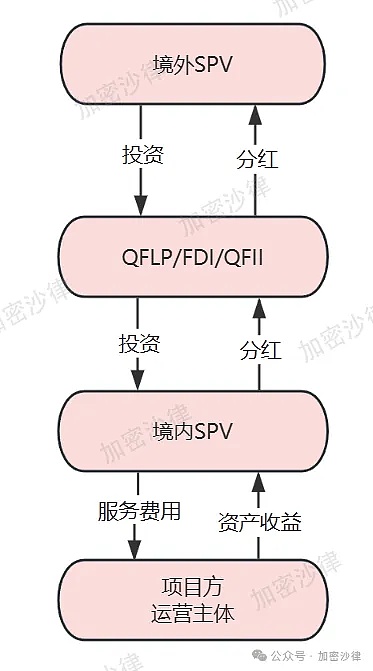

(III) Compliance with fund circulation

Due to the strict foreign exchange control implemented in my country, the funds raised by issuing RWA overseas cannot be directly transferred to the actual operating entity in China. The compliance team needs to design a framework and path for the collection and circulation of overseas funds.

According to the project experience of the Crypto Salad team, after the RWA project completes financing by issuing tokens overseas, the funds of the overseas SPV will generally be collected through the fund channel and finally transferred to the actual operating entity. There are three options for the funding channels in this structure:

1. QFLP (Qualified Foreign Limited Partner)

2. FDI (Foreign direct investment)

3. QFII (Qualified Foreign Institutional Investor)

When designing the capital flow structure, the compliance team generally needs to consider the following factors: tax burden, entry threshold, procedural requirements, compliance costs, etc. In the process of actually implementing the project, the project team must also pay attention to compliance first. The preparation of application materials for different funding channel entities, window opinion responses, and the adjustment and improvement of the corresponding framework all require the full support of a professional lawyer team.

(The above picture is a schematic diagram of the RWA project funding channel, for reference only)

It only represents the personal views of the author of this article and does not constitute legal advice or legal opinions on specific matters.

比特币昨日触及 69,546 美元高点后回落,盘中最低跌至 66,500 美元,令部分投资者出局。以太坊跌幅更大,回到 2,640 美元的关键盘整区。市场在短期内面临健康调整或是深度回调,仍有待观察。

AlexMeta is using facial recognition technology to block scam ads that misuse celebrity images and help users recover their accounts faster. The system compares faces in ads with real profile pictures to detect and stop fraud in real time.

Weatherly

Weatherly去中心化物理基础设施网络(DePIN)正在通过创新技术为 Web3 游戏带来深远变革,赋予玩家更多自主权,提升互动性与经济可持续性。DePIN 让玩家真正掌控游戏资产和治理权,创造沉浸式体验的同时促进社群合作与新的收入模式。

Miyuki

MiyukiElon Musk's AI startup, xAI, has launched a Grok API for its chatbot, allowing users to access its features for a fee, but questions remain about the model's capabilities. Grok aims to provide less restricted responses than competitors and is integrated into the X platform, although it faces scrutiny over data privacy and environmental issues.

Anais

AnaisA phishing scam targeted users searching for "Soneium," a blockchain project by Sony, by leading them to a fake website that stole their crypto assets. The fraudulent ad appeared legitimate on Google, but redirected users to a site designed to drain their wallets.

Joy

JoyIndonesia's regulatory agency, Bappebti, has extended the deadline for crypto exchanges to obtain a Physical Crypto Asset Trader (PFAK) license until the end of November 2024. This extension allows exchanges more time to comply with updated regulations and aims to strengthen the digital asset market in the country.

Anais明尼阿波利斯联储发布报告称,禁止或对比特币征税有助于维持美国的永久预算赤字,引发华尔街强烈反对,相关人士引用1996年的论文为比特币辩护。币圈看好特朗普胜选,认为他上台后将推动设立比特币国家储备,目前其胜率已飙升至65%。

Alex普京宣布,金砖国家联盟成员,包括巴西、俄罗斯、印度、中国和南非,将采用加密货币推动投资与经济发展。这一举措被视为联盟的重大转折,可能加速全球“去美元化”进程。

MiyukiKomainu is making its first acquisition by purchasing Singapore-based Propine Holdings, gaining a Singapore Capital Markets Services License and positioning itself for a future Major Payment Institution license. Though financial details were not disclosed, this marks a key step in Komainu’s expansion in Asia.

Catherine

Catherine明尼阿波利斯联储主席卡什卡利称比特币主要用于毒品交易和非法活动。然而,最新的区块链分析显示,非法交易仅占加密货币使用的极小部分。加密领域的专家纷纷反驳,指责卡什卡利对加密货币的误解和错误言论。

Weiliang

Weiliang