With the new segmentation metrics we introduce in this article, we are now able to analyze in a more detailed way the specific moments when investors suffered severe unrealized losses and “throw up their hands” to the downside. In addition, we introduce a new framework to analyze and evaluate the exhaustion of selling potential among different investor groups over multiple time frames.

Abstract

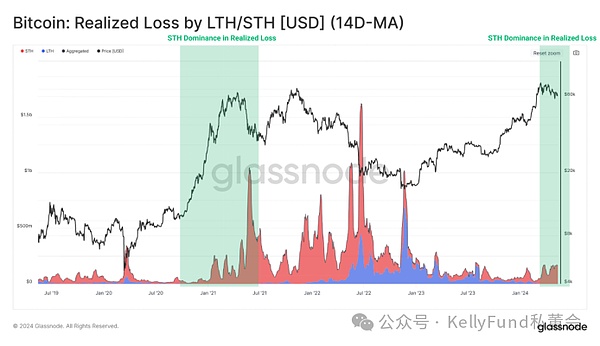

During the bull market, long-term investors usually achieve high profits. Therefore, realized losses mainly come from the short-term holder group, and their investment activities can tell us a lot about the market turning points during the selling events.

Given that market turning points unfold from the inside out, we construct a framework using the new segmentation metrics by holding period to describe the exhaustion of sellers among the investor groups within the day, week, and month.

Within this framework, we use on-chain metrics to assess the unrealized and realized losses of different categories of investors to evaluate their investment decisions during the current market downturn.

Building a “Seller Exhaustion” Framework

When we evaluate the market conditions of the Bitcoin bull run in a macro timeframe, it is not difficult to find that the price action at this time is generally characterized by volatile rises accompanied by corrections and consolidations. All investors know that financial markets do not just rise over time, and such volatile markets cause a cat-and-mouse game between supply and demand, which triggers local and global market correction events.

We first evaluate the realized losses of long-term and short-term holders. We can observe that the realized losses suffered by long-term holders occur almost entirely during the macro recession cycle. In contrast, in recent times, recent buyers have locked in losses at various times in the market - indicating that such losses are almost entirely from short-term holders, and such losses from short-term holders are usually the main source of losses during bull markets.

In this report, we will use the fact that the realized losses in the market are almost entirely from short-term holders to determine when sellers may have exhausted their investment potential. Our main goal is to identify market inflection points during corrections and consolidations in bull-dominated market trends.

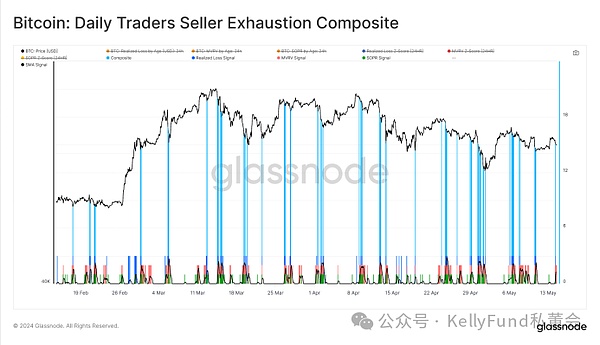

Here, we define seller exhaustion as the point at which an oversold event occurs, and the arrival of this point in time indicates that most of the people who intended to sell have completed the sale of the asset. Since there must be a buyer to match every seller in the trading pair, we can see what buyer demand absorbs the seller's selling, which helps us identify local bottoms in the market.

The impact of turning points in market trends tends to start from smaller time frames (minutes to hours) and then spread to larger time frames (days to months). To capture this spread effect, we will use the newly released holding time segmentation indicator to separate two different groups of investors from the short-term holder group:

To model the time points when investors are under extreme economic stress, we will use three profit and loss indicators to help us understand the severity of this economic stress experienced by investors:

MVRV ratio: assesses the unrealized profits or losses held by investors in this group.

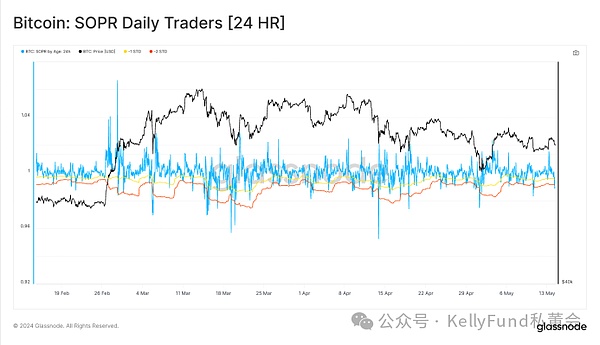

SOPR: Assess the extent of profit, loss or loss of investors in the group.

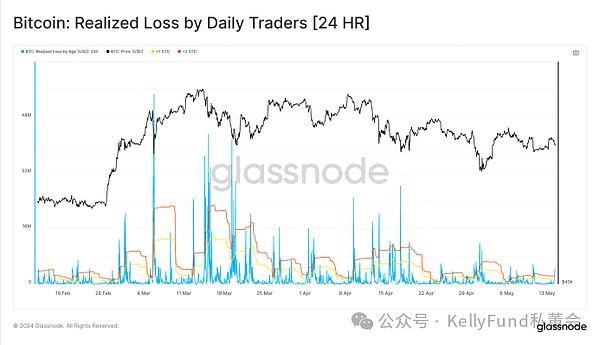

Realized Loss: Assess the extent of losses of investors in the group in US dollars.

Day Traders

First, let's assess the day trader group and analyze their investment activities using the corresponding 24-hour segment indicators.

Day traders are essentially the fastest-acting investor group. They are most sensitive to spot prices and can react almost instantly to any price fluctuations. Therefore, this group will generate a lot of signals of weakening selling power, but due to the large changes in the selected time period, this part of the data will generate more "noise" and interfere with the accuracy of the data we want.

We first evaluate the MVRV Z-score for the day trader group (we set 90 data backtracking points to fully evaluate this data indicator). We can see that due to intraday price fluctuations, the indicator has continued to decline from its original high value, affecting the unrealized profits and losses of the day trader group.

Throughout the market price correction, we have been committed to looking for moments of seller exhaustion, and the MVRV Z-score is the key indicator we use - when the score is below the mean -1σ, we will highlight the current time points. These marked time points are the time points when the unrealized losses of day traders increase, and are also the points where statistically day traders are under heavy investment pressure. Next, we will combine the SOPR indicator to assess whether the day traders have taken action to deal with the unrealized financial pressure and whether those losses have become actual losses. Third, we will analyze the Z-score points below the mean -1σ separately, because the emergence of these extreme values represents a small-scale collapse of their confidence and the emergence of greater selling pressure in the market at the same time.

Finally, we can further clarify the above observations by evaluating the realized losses in US dollars suffered by the day traders, so as to assess the size of the selling pressure. Here, we apply a similar Z-score framework to assess the realized losses of day traders over a 24-hour period, using the same approach as before - by finding specific points where the Z-score is above 2σ of the mean, we are also able to identify periods of time that represent periods of significant setbacks in day traders' confidence.

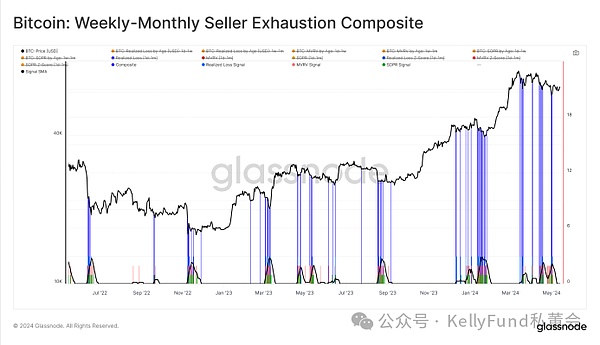

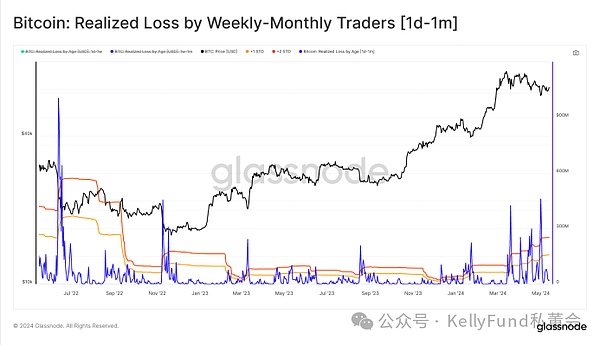

Weekly-Monthly Traders

Now turning our attention to the weekly-monthly group, the first thing we observe is a significant slowdown in the oscillations in market signals - this is what we would expect given the longer time horizons we have been trading. This slowdown has undoubtedly smoothed the average cost basis of the weekly-monthly group. We also see that this group is less sensitive to price changes and does not buy or sell as frequently as day traders, but they are also more likely to experience volatility. Because during their holding period, asset prices always fluctuate around their cost basis

By studying the MVRV Z-scores of weekly-month traders, we can see that compared with day traders, the MVRV Z-scores of weekly-month traders are not as sensitive to market price fluctuations as the former. Therefore, their MVRV indicator fluctuations are also more gradual than the former, and the overall market signals generated are less, but at the same time, the "noise" is also less severe.

The figure below highlights the situation where the MVRV Z-score of weekly-month traders is below the average (i.e., the Z-score is negative), which we regard as an important indicator because it indicates that a large number of unrealized losses have been transferred to the weekly-month traders. Similar to the previous analysis, we use the Z-score of the SOPR ratio to confirm whether the weekly-monthly traders will experience a similar collapse of confidence when their financial pressure exceeds a certain threshold, thereby selling their stocks and cashing out their losses. Similar to the MVRV ratio Z-score, we extract these specific time points for separate analysis when they are below the average. We find that, from this perspective, we also find a similar diffusion effect of realized losses spreading from shorter time periods to longer time periods. At the end of our analysis, we can use the Z-score of realized losses to further verify. In this analysis of the indicator, we define the Z-score values above the mean +2σ as outliers and use them to identify the market locations where the weekly-monthly traders have incurred significant losses (the losses incurred are also denominated in USD).

Z-score framework to evaluate realized losses. In this analysis of the indicator, we define the Z-score values above the mean +2σ as outliers and use them to identify the market locations where the weekly-monthly traders have incurred significant losses (the losses incurred are also denominated in USD).

Summary

The diverse on-chain data provides analysts and investors with a high degree of transparency into the different positioning, incentives, and actions of different market participants. We can use these tools and indicators to build models to assess how investor behavior is affected by market prices and how it changes accordingly.

Using new segmentation indicators, we can further segment short-term holders with different holding periods on a time scale. We then use a combination of three on-chain indicators that describe the profitability of these investor groups to identify specific time points that indicate that their investment confidence may collapse or their investment potential may exhaust, which are often accompanied by local market lows. When identifying sell-side exhaustion points, this analytical framework can help us predict what motivations and behaviors investors usually have.

JinseFinance

JinseFinance