Circle cuts 'marginal' amount of staff to strengthen balance sheet: CoinDesk

Circle laid off some employees this week to strengthen its balance sheet.

TheBlock

TheBlock

Original author: FTX_Benson

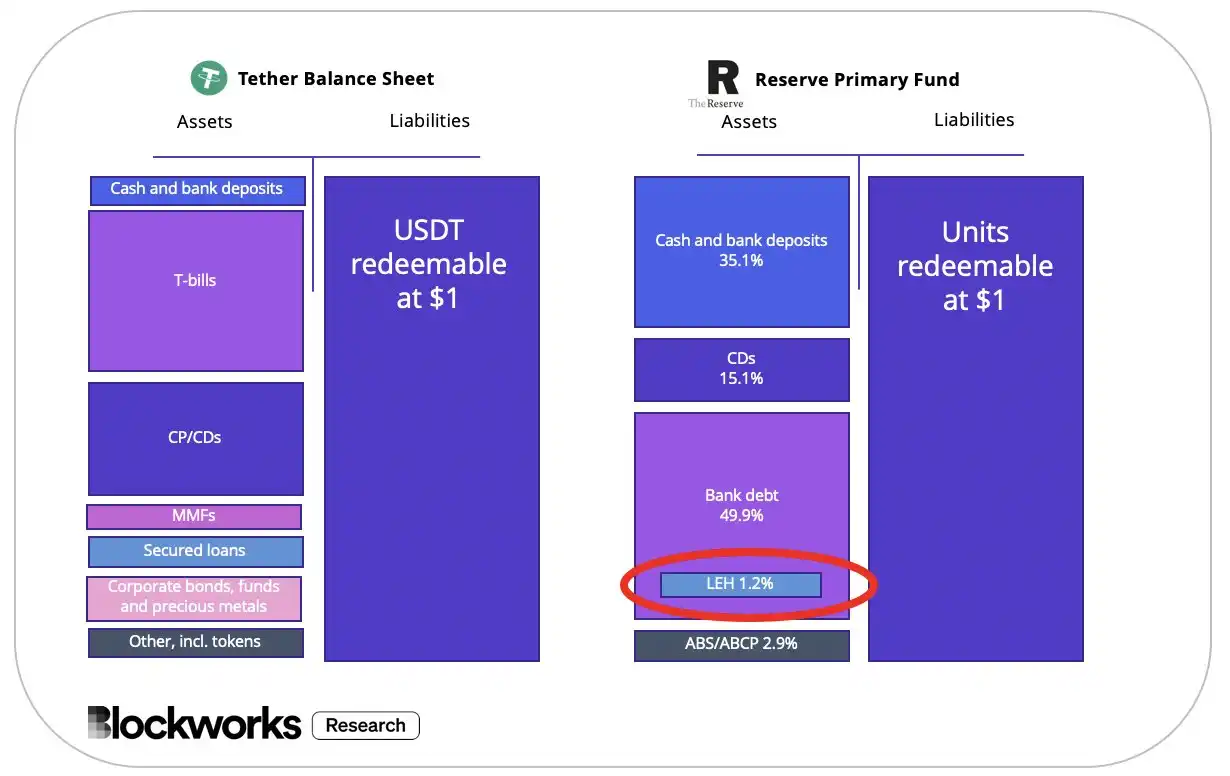

Let’s take a look at the asset reserve composition of USDT first. In fact, the asset reserves of all Stablecoin issuers are similar to the composition of money market funds. They are mainly cash, high-quality short-term bonds and bills.

Back in 2008, Reserve Primary, the largest money market fund at that time, had a size of US$63 billion, and it held about US$78 million in short-term bonds of Lehman Bank (accounting for only 1.2% of total assets).

It was this negligible exposure that caused panic in the market. Because the news of Lehman Brothers' bankruptcy was too sudden, Reserve Primary had no time to deal with Lehman's short-term bonds. No one wanted to buy or sell these bonds, so it was impossible to assess their residual value. As a result, they have no way to assure investors that their 100 cents are equivalent to 1 dollar.

On September 16, 2008, Reserve Primary announced that it had only 97 cents left. It broke the public's perception that the value of money market funds is always $1. Subsequently, the investor's redemption frenzy caused Reeserve Primary's asset size to shrink by 60% in 2 days, making the fund have to announce a one-week suspension of redemption.

The fall of Reserve Primary led to the worst investor panic in modern financial history, as investors withdrew as much as $123 billion from money market funds over the next two weeks.

To understand whether USDT will be thunderstorms, two questions must be answered first:

1. What is the liquidity of the USDT asset reserve quality?

2. Is it possible for USDT to experience a huge wave of redemption like the money market funds in 2008?

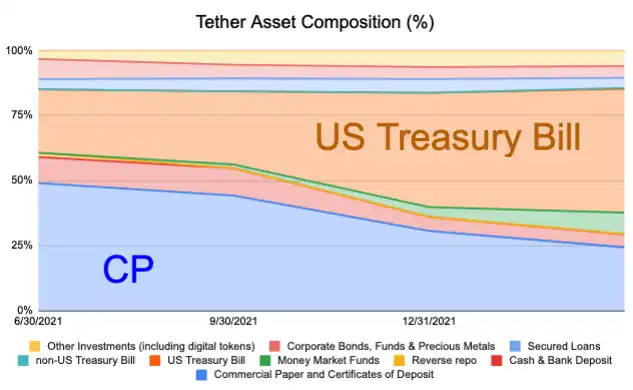

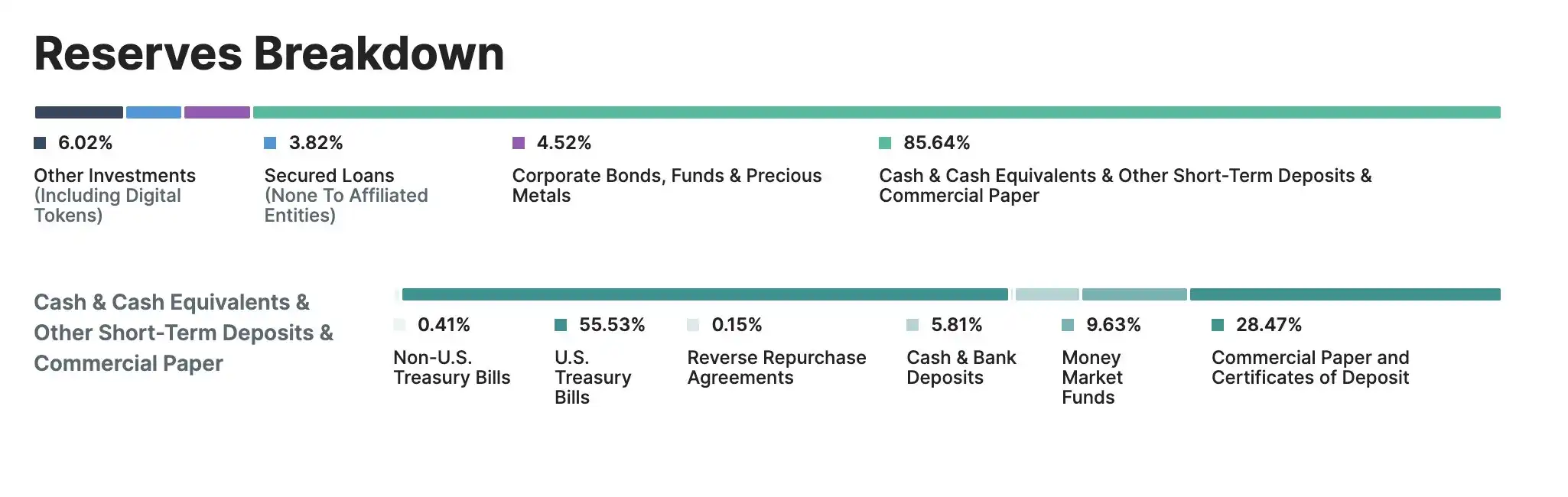

To answer the first question first, the quality of USDT asset reserves has been improving all the time. Originally, half of them were CP (commercial paper), and this part was slowly replaced by T-Bill (US short-term treasury bonds).

CP vs T-Bill Ratio:

2Q21: 49%, 24%

3Q21: 44%, 28%

4Q21: 31%, 44%

The 2022Q2 report has not yet come out, but according to Tether CTO @paoloardoino, Tether has reduced its CP by about half after 2022/3/31, and currently only holds 8.4 billion US dollars in CP, which means that the proportion of CP has dropped again At around 13%, their long-term goal is to reduce the CP exposure to zero.

Since the USDT circulation has not changed much before 2022/5, it is reasonable to guess that the original CP position has been transferred to other assets (high probability is T-Bill).

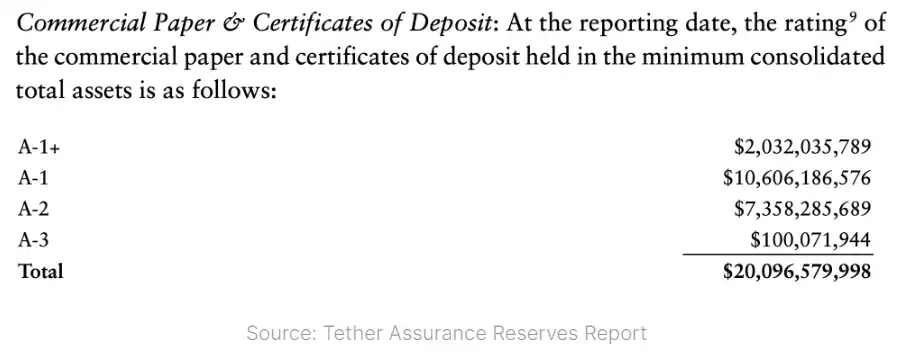

Regardless of T-Bill, the quality of CP held by USDT is also very good, and the proportion of CP rated above A-3 has been increasing. In the 2022/3 audit report, it was revealed that 99.5% of USDT's CP ratings were above A-3.

There is a proverb in English: action speaks louder than words (action speaks louder than words).

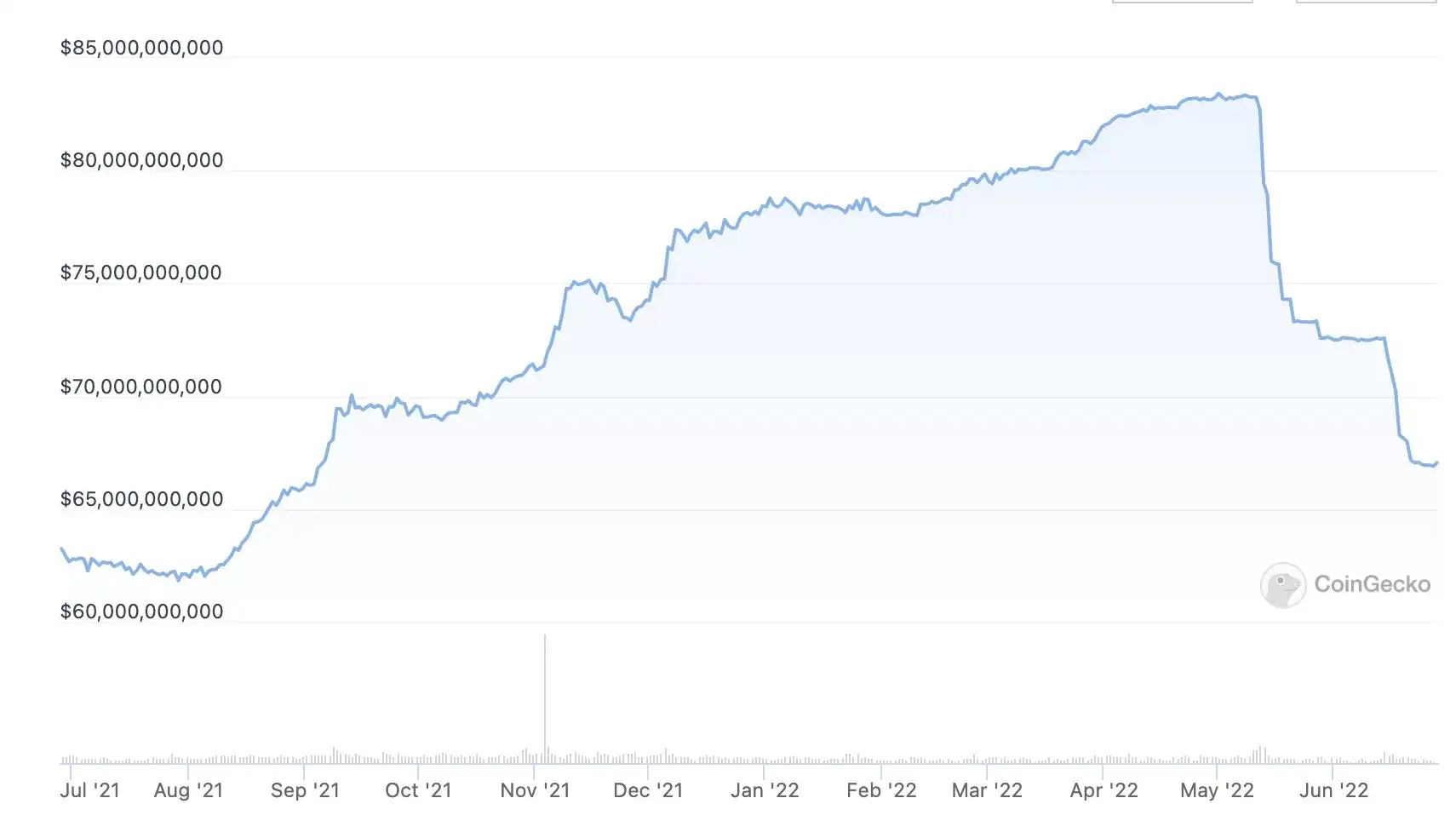

The best way to express liquidity is the stress test of a large number of redemptions. In the past month or so, USDT has redeemed 17 billion US dollars, and the circulation has decreased by 20% (83 billion --> 66 billion), of which 10 billion redemptions occurred When UST collapsed and the overall market was most panicked (5/12-5/15).

From the above, we can know:

· The quality of USDT reserve assets has been improving, and the CP ratio, which was criticized in the past, has been reduced to about 13%.

· The proportion of T-Bill continues to rise, and is currently close to 50%, and the audit report for the new quarter is likely to exceed 60%.

· USDT only holds investment grade CPs, and 99.5% of CPs are rated above A-3.

· USDT has proven its ability to redeem a large amount in a short period of time. The liquidity of USDT is even better than that of some banking units based on the performance of the 5/12-5/15 redemption wave.

Then come to the second question, assuming that the market is super panicked and there is a huge wave of redemption (for example, more than 80% of the circulation is redeemed within a week), will USDT be decoupled?

The answer is that there is a high probability that yes, quick redemption means that a large number of assets need to be sold in the short term, and a slight price slippage will cause decoupling. In fact, all Stablecoins cannot pass this level. If such a super black swan really happens, it will be useless for you to switch to USDC.

So a better way to ask the second question is, how likely is the super redemption wave to happen? Is it possible that USDT will suddenly be overwhelmed by a large number of redemptions like the money market funds in 2008?

First of all, the securities of money market funds are investment tools, and they have no other purpose other than yield. When there is a crack in confidence, all investors will want to flee.

But USDT is different. As a veteran Stablecoin, USDT has far surpassed the role of Stablecoin itself . All USDT trading pair market makers must hold USDT to operate (regardless of contract or spot, this volume is at least 10 billion U.S. dollars. ). Many OTC withdrawal channels and even black market transactions must rely on USDT.

To put it simply, compared with money market funds that may collapse due to the collapse of confidence, a large part of USDT will not escape (or cannot escape) at all. I roughly estimate that this proportion accounts for at least USDT issuance. About 20% of the amount.

In addition, not everyone can apply for the redemption of USDT. Only institutions that have passed the whitelist verification can directly trade with Tether and exchange USDT for US dollars. Therefore, when the extreme market appears, it is unlikely that USDT will be wiped out in the short term, and the price will slide to the sky.

85% of USDT's reserves are cash & cash equivalent, which can be regarded as the part that can be quickly sold for cash in a short period of time, and more than half of the 85% are T-Bill with high liquidity.

We assume that the market makers of USDT pairs, together with some people who have to hold USDT, account for 20% of the total circulation (in fact, it should be higher). These people cannot escape, and they can only feel numb in the face of Fud.

Assuming that the remaining 80% of the circulation wants to escape, the escape process will be:

1. USDT depegged due to selling pressure.

2. Arbitrageurs step in to buy USDT and exchange USD with Tether.

Only if the arbitrage buying of 2 is not enough to resist the selling of 1, it may lead to the spread of panic and cause a larger-scale decoupling.

Since Tether's redeem process has been smooth and has not been closed since its release, this decoupling is usually very short-lived. Even at the moment of extreme panic when UST collapsed on 5/12, USDT was only temporarily de-anchored by 0.95, which is very short. Bounce back soon.

Not only arbitrage institutions that can directly trade with Tether will buy it, but other speculative buying in the market that is not afraid of death will also intervene, just like UST has a lot of people who don't arbitrage at all just want to bet that he will get back $1. The buying made UST dragged on for a week before it really exploded and fell below 0.5. This kind of speculative buying will only be stronger in USDT. Since 2017, the industry has experienced USDT Fud too many times.

To sum up, will USDT have a thunderstorm? I think the probability is very low. Those hedge funds have a high probability of losing the short interest, but if they are randomly fud out of a small hole (let's say ~0.95), they will still make money if they close their positions in time. So they're trying their best at Fud, get it?

Circle laid off some employees this week to strengthen its balance sheet.

TheBlockThe outstanding loans of $2.8 billion has around 30% of lending made to related parties, including parent company DCG.

Market Watch

Market WatchThe valuations given to some of the tokens on the balance sheet are fiction.

Ledgerinsights

LedgerinsightsThe Financial Times has seen a copy of an FTX balance sheet showing that the bankrupt crypto exchange had only $900mn of assets it could easily sell.

Financial Times

Financial TimesSaylor believes that bitcoin is the answer to inflation as the Fed prepares to meet on Sep. 21, 2022.

Beincrypto

BeincryptoThe crypto contagion only hurt entities that poorly managed their treasuries, but didn't affect the underlying blockchain technology, he said.

Cointelegraph

CointelegraphCelsius Network had its first limited withdrawals back on June 13th, and it had taken about one month from that ...

Bitcoinist

BitcoinistOctagon Networks, a global cybersecurity company, announced it would adopt a Bitcoin standard, offering half-price discounts for Bitcoin payments.

CointelegraphThe business intelligence firm now owns a total of 129,218 BTC.

CointelegraphMacro-induced mayhem costs Bitcoin bulls dearly as Ethereum also loses key $3,000 support.

Cointelegraph