Author: David Christopher Translator: Block unicorn

BlackRock's iShares Staking Ethereum Trust ETF (ETHB) began trading on Nasdaq today. This is the company's first staking fund, quietly solving a problem that has plagued institutional Ethereum investors since the launch of spot ETFs.

For the first time, Wall Street can access ETH in the way it's touted: a productive, yield-generating asset.

The Initial Disconnect

From the beginning, spot Ethereum ETFs suffered from a mismatch problem.

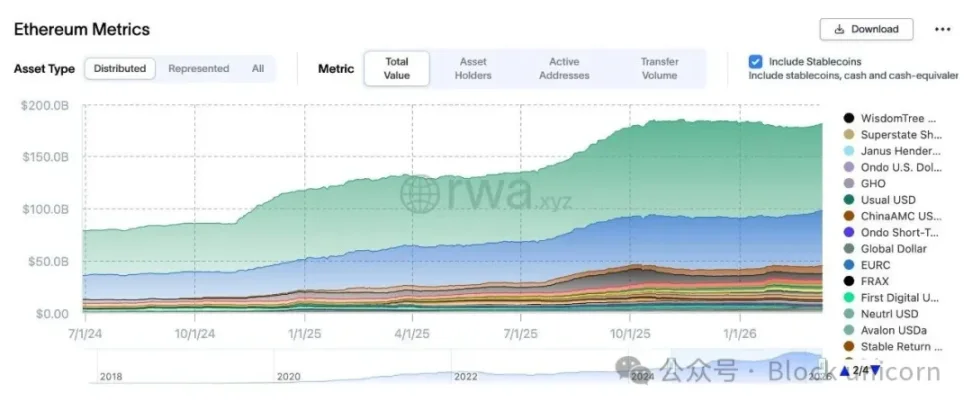

Ethereum has long been touted as an "internet-native bond"—scarce (with an annual issuance cap of 1.5%), high-yield (3-5% annual compound interest), and embedded in the settlement layer of new financial systems (stablecoins and tokenized assets). Ethereumize formalized this framework last year: ETH is simultaneously digital oil, productive collateral, and a reserve asset. Even though this claim seems somewhat far-fetched, it still works, as we previously saw with DAT promoting ETH as a stablecoin investment vehicle. However, the product itself hasn't delivered. Spot ETFs have failed to provide returns. Investors gained price exposure but couldn't experience Ethereum's economic engine. We were selling a productive asset, ultimately giving institutions a package devoid of productivity. Bitcoin doesn't have this problem. The essence of BTC's value proposition lies in its simplicity: a store of value. Simply hold it. Spot trading provides the full value. Ethereum's proposition is different. Staking is an integral part of Ethereum assets. Holders benefit from the network economy and earn the compound interest that underpins its core principles through staking. Spot ETFs cannot provide this. While this isn't the only reason, this dynamic has resulted in a significant lag in institutional investor inflows into Ethereum (ETH). Currently, IBIT holds over $55 billion in market capitalization, while ETHA's is only around $6.5 billion. Admittedly, part of this gap reflects Bitcoin's first-mover advantage and clearer narrative. But part of the reason also reflects flaws in the product itself. Institutional investors are attracted by Ethereum's upside potential but end up with a diluted version of the asset. Wall Street has already entered the fray. This poor asset-related performance often masks the actual institutional adoption of Ethereum since the launch of spot ETFs in July 2024. The supply of RWA on Ethereum has grown approximately sevenfold. The supply of stablecoins has also more than doubled. Wall Street increasingly views ETH as infrastructure, a conduit for stablecoins and tokenized finance, rather than as a standalone trading instrument. RWA growth on Ethereum from July 2024 to present. BlackRock's BUIDL fund, Franklin Templeton's FOBXX, and a growing number of tokenized money market products use Ethereum or its L2-based settlement system for settlement. Banks and SWIFT are also settling on testchains. While ETF flows have been disappointing, institutional investor participation is actually expanding. However, some of these flows are not driven by demand for ETH, but rather by a lack of suitable ETH access channels. Institutional investors can hold price exposure to ETH, but cannot participate in the network they increasingly use, are using, or at least finally understand its value. ETHB solves this problem. For the first time, institutional investors have a truly regulated form of encapsulation that aligns with the Ethereum philosophy.

Ethereum stablecoin growth since July 2024.

Structural Impact

This matter is more important than ETHB itself.

Previously, investors outside the cryptocurrency space who wanted to effectively invest in Ethereum (ETH) had to use some workarounds: mainly structures like DAT, which allowed for free staking, re-staking, and DeFi usage, but whose value was not directly related to the assets held.

These structures exist in part because institutional investors cannot directly participate in staking within their authorized scope. This has changed with the launch of staking ETFs. Funds that previously had to go through intermediaries can now flow directly into the Ethereum market. Current Status Quo According to the DeFi Report, most cyclical indicators show that ETH was in the fair to deep value range when ETHB launched. MVRV is below 1, meaning the market is at a loss from a total cost perspective. Profit supply is lower than during the capitulation sell-off of 2022. The current cycle price has barely surpassed the 2021 high (apologies for the reminder), and has been oscillating within the previous high range without breaking through. Historically, the current price is in a highly attractive compression state. As I mentioned earlier, this poor performance cannot be simply attributed to the lack of a staked ETF. Ethereum's L2 roadmap optimizes scale and user experience, not L1 fees. Blobs make Rollup pegging inexpensive and break the fee burn mechanism that once underpinned deflationary rhetoric. Admittedly, Ethereum as a network has improved, but its investment prospects have become more unpredictable. However, its monetary structure has never collapsed. Annualized issuance is around 0.8%, roughly in line with Bitcoin's inflation rate. Now, various factors are converging again. The number of institutional users is growing significantly and consistently, and RWAs, stablecoins, and tokenized funds are thriving on Ethereum. Staking mechanisms have finally matured, and prices have reached reasonable levels. For years, Ethereum has been marketed to institutional investors as a yield reserve asset and settlement layer for the tokenized economy. This story has been continuously refined, formalized, and repeated: it constantly peddles the idea to institutional investors who clearly see the value in the Ethereum network but are unable to participate in the Ethereum economic plan. Now, Ethereum's packaging finally aligns with this theory, and ETHB will be a test. We will wait and see if Wall Street truly endorses the idea being sold about Ethereum as an asset.

JinseFinance

JinseFinance