Author: Thejaswini M A Translator: Block unicorn

Foreword

We tried everything.

NFTs were supposed to attract creators. Web3 games promised to bring blockchain to the masses. Social protocols like Farcaster and Lens promised a decentralized future for digital communities. Zora aimed to prove that content could become a financial asset. Friend.tech turned social capital into something that could actually be traded. Memes—well, nobody says they're building civilizations, but everyone says they'll bring the next wave of retail investors.

NFTs were originally intended to attract creative talent. Web3 games promised to bring blockchain to the masses. Social protocols like Farcaster and Lens heralded a decentralized future for digital communities. Zora aimed to prove that content could become a financial asset ...>

Prediction markets integrated through Kalshi. You can bet on elections, Fed decisions, and sports outcomes without leaving Coinbase. The cryptocurrency portion is completely transparent.

Perpetual futures for international users. Lending supports borrowing up to $5 million against Bitcoin (BTC) and up to $1 million against Ethereum (ETH). Additionally, a primary token sale will be launched, allowing retail users to purchase tokens before their official listing via USDC.

Brands can create their own branded stablecoins backed by USDC. Stablecoin payment functionality is already embedded in Shopify, Checkout.com, and PPRO, launching in 2026.

UK savings accounts offer an annual interest rate of 3.75% and are guaranteed by the FSCS. They are applying for a National Trust charter, which will grant them greater banking authority. Coinbase is building infrastructure to help everyone access the blockchain. This includes not only a super app for its users, but more importantly, it provides Rails backend support for institutions, fintech companies, and traditional banks venturing into the cryptocurrency space. Coinbase hosts over $7 billion in on-chain assets. cbBTC is the second largest asset, valued at approximately $2.5 billion. Its integration with Morpho shows that $2 billion in collateral has supported over $1 billion in loans. Robinhood, on the other hand, is taking the opposite approach: initially a stock trading app, it is rapidly evolving into a full-stack cryptocurrency platform. Their features include: ETH and SOL staking for US users; perpetual futures with up to 7x leverage for European users; and over 1,000 tokenized stocks, US stocks, and ETFs for EU clients, supporting 24/5 trading with zero commission. Their Ethereum Layer-2 blockchain, "Robinhood Chain," built on Arbitrum, is currently on the testnet. As of Q3 2025, the assets under custody for crypto assets reached $51 billion. In the past twelve months, the notional trading volume of cryptocurrencies reached $232 billion. An AI assistant called Cortex provides insights and market analysis for Gold members. A credit card that automatically converts cashback into cryptocurrency. Staking is positioned as a "core feature" and a major driver of user engagement in 2026. They acquired Bitstamp to strengthen their global cryptocurrency infrastructure. They are expanding into Indonesia. They are developing Robinhood Social, a platform where traders can post actual trades and profit/loss information. They already have the infrastructure for new banking, including direct deposits, credit cards, and cash management, and are layering cryptocurrency on top of that. Then there's the cryptocurrency enthusiast's favorite: Hyperliquid processed $2.8 trillion in perpetual futures trading volume in 2025. The company made it into the Forbes Fintech 50 with zero funding. This is arguably the most successful consumer product case in the cryptocurrency space. However, Hyperliquid isn't a groundbreaking consumer-facing technology, but rather a success story within the cryptocurrency space. It serves users already familiar with perpetual futures, leverage, and order book dynamics. Its trading volume primarily comes from traders already in the cryptocurrency space seeking better execution. Hyperliquid simply provides existing users with a better trading platform. What are we missing? What should an ideal cryptocurrency consumer application look like? Don't be vague, be specific. An invisible wallet. No need to worry about mnemonic phrases. Social recovery or biometric security. Progressive custody starts with ease of use, gradually increasing security as your balance grows. The technology already exists: account abstraction, access keys, and smart contract wallets. However, adoption has been slow because developers prioritized the purity of decentralization over user experience. Seamless fiat currency deposits and withdrawals. Instant settlement. No need to wait three to five business days for ACH transfers. No need to understand the difference between USDC and USDT. No minimum deposit requirement. Simply link your bank account to transfer funds. No obscure jargon. "Send Sarah $50," instead of "Enter recipient address and specify gas limit." Natural language interaction, understanding user intent. Error recovery functionality allows you to undo transactions or cancel pending operations. A clean and intuitive interface, not as complicated as operating a spaceship. All operations can be completed with a single click—payments, exchanges, earnings inquiries, social features, and more. Introducing crypto concepts step-by-step to users who want to learn, while providing a completely abstract interface for those unfamiliar. A consumer-facing trust layer. AI-driven risk warnings alert you before you approve a transaction, warning that "this looks like a scam." Automated portfolio management that optimizes DeFi yields. Automated processes for seamless tax reporting. The assurance that ordinary people expect from financial products. Compliance features are built into the system but not visible to users. Selective disclosure allows you to share specific balances without revealing your full wallet. Transaction privacy can be protected by blocking transfers when necessary. Identity protection uses pseudonyms by default. Data sovereignty allows users to control all their personal information. A powerful narrative explaining why this matters, without any belief system. Not "overthrowing the financial system" or "creating your own bank," but "it does what you're already doing better." It shouldn't feel like "using cryptocurrency," but rather like a better banking app. The problem is that most cryptocurrency apps are developed, tested, and funded by cryptocurrency practitioners. When your test users have MetaMask installed and are familiar with gas fees, you don't feel the friction that hinders other users from adopting it. Cryptocurrency solves problems that most people in developed economies don't have. Self-custody of funds and censorship resistance are indeed very important principles. But for those with normal bank accounts and stable currencies, these are abstract threats, not everyday pain points. The marketing of cryptocurrency focuses on "you should want it because of its potential impact," rather than "it provides tangible benefits right now." This argument simply doesn't hold up in competition with Venmo and Cash App. What We've Overlooked

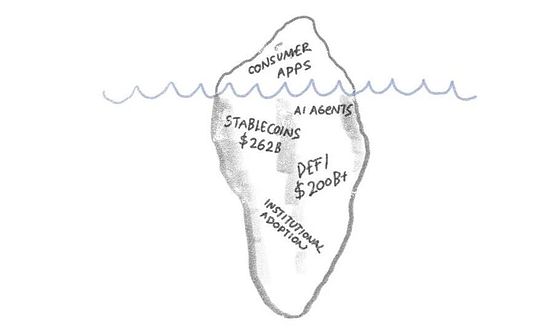

We often think cryptocurrencies failed because they lacked cool consumer applications. But think about it: their infrastructure is incredibly mature.

Stablecoins have proven effective. They are fully functional infrastructure, transferring real value across borders daily. Security has improved dramatically. Smart contract auditing is now standard practice. Multi-signature wallets are widespread. Insurance protocols are also available. The catastrophic hacks of 2021-2022 have significantly decreased in frequency as the industry has learned its lesson.

DeFi trading platforms are extremely efficient. Protocols like Uniswap, Aave, and Compound can handle billions of dollars in transactions with minimal downtime. The total value locked on DeFi platforms exceeds $300 billion. Institutional investors are leveraging these platforms for efficiency.

Institutions are leveraging this technology. BlackRock has launched a tokenized money market fund. JPMorgan Chase is processing blockchain-based repurchase transactions. Traditional financial institutions are also quietly using crypto infrastructure because it is more efficient than traditional systems in certain application scenarios. Liquidity is deeper than ever before. The bid-ask spreads that plagued early DeFi have narrowed significantly. Arbitrage bots ensure efficient price movements across different trading venues. Professional market makers provide ample liquidity. Institutional users are adopting cryptocurrencies before retail users. This is unusual, but crucial. If you believe that artificial intelligence represents the future, then AI agents need stablecoins. They need programmable settlement systems. They need cryptocurrency infrastructure. Chris Dixon also agrees that AI agents need programmable money, which traditional banks cannot provide. As AI becomes more widespread, cryptocurrency infrastructure will become an essential infrastructure. Therefore, infrastructure may be more important than hype. The foundation is already there; what is lacking is not technology. Cryptocurrency consumer apps will eventually prevail, but only if they stop trying to masquerade as cryptocurrencies. The truly successful apps won't require people to "use cryptocurrency," but rather will offer genuinely better solutions to the problems people already face: higher savings returns, faster payments, lower transfer costs, portable identity information, and true ownership. Bank accounts will feel familiar, and the interface will be very intuitive. In the background, stablecoins will handle settlements, smart contracts will execute, and the blockchain will provide final confirmation—users won't have to worry about anything. Every generation creates tools they don't fully understand. Those who laid the transatlantic telegraph cable in 1858 thought they were simply building a faster way to transmit information. They probably never imagined they were constructing the nervous system of the global economy. We often judge new infrastructure based on the first things people build on it. And the first things are almost always wrong. They are merely imitations of the old in the guise of new technology. Horseless carriages, moving photographs, electronic newspapers—these are examples. The real transformation happens later. When someone who has grown up with the infrastructure builds something that couldn't exist without it, something the original builders never imagined. Ten years from now, the applications they develop will be completely different from what we're discussing on cryptocurrency Twitter right now. It won't be an improvement on existing products; it will be something we can't yet describe in words. Our task now is not to build that thing. We can't. Our task is to ensure the infrastructure is in place, functioning properly, and usable by those who will be able to develop on it without reading a white paper in the future. Finance is the means to achieve our goal. Because it empowers enough people with the necessary tools, enabling the true builders—those we haven't yet encountered—to begin action. This is the strategy that truly works. It's neither transformation nor surrender. We're simply constantly distracted by trivial matters. The most important cryptocurrency applications haven't yet been conceived. And that's my most optimistic view of the industry.

Anais

Anais